Strategy Retires Convertible Bonds Early in Major Capital Structure Move

On May 14, Strategy filed an 8-K disclosing the repurchase of approximately $1.5 billion face value of its 0% Convertible Senior Notes due 2029. The company paid an estimated $1.38 billion in cash - below par - to retire the position in privately negotiated transactions. The notes were cancelled on settlement around May 19.

What Was Repurchased

The 2029 convertible notes were issued in November 2024 at a $3 billion notional size, 0% coupon, with a conversion price of $672.40 per share. At the time of the repurchase, MSTR was trading near $183 - roughly 73% below the conversion threshold. The equity optionality embedded in these notes had long since been priced out of the instrument. What remained was a fixed cash obligation due in 2029, with no realistic conversion path.

Buying back $1.5 billion face value at $1.38 billion eliminates approximately $120 million in future liability. More directly, it removes the shares those notes could theoretically convert into - reducing potential dilution and increasing Bitcoin per share for existing common holders. The mechanism is not a traditional stock buyback, which retires current shares immediately. In a convertible-heavy structure like Strategy's, retiring the convertible is the functional equivalent: anti-dilution capital allocation at a discount to face value.

Approximately $1.5 billion of the 2029 tranche remains outstanding following settlement. Strategy held 843,738 BTC at an average cost basis of approximately $75,700 per coin at the time of the announcement.

The Funding Question

Strategy named three potential funding sources in its disclosure: existing cash and liquid assets, proceeds from its ATM equity programmes (both MSTR common and STRC preferred), and Bitcoin sales. The actual split has not been confirmed publicly, but the most likely composition is MSTR ATM proceeds as the primary channel, supplemented by a modest Bitcoin sale.

MSTR common equity (ATM). At prevailing mNAV multiples, issuing common stock to fund a debt retirement is mechanically accretive on a per-BTC basis: shares are issued above net asset value, proceeds retire debt below face value, and the residual effect is an increase in Bitcoin per share for remaining common holders. The MSTR ATM is Strategy's highest-velocity capital channel and the most probable primary mechanism here.

Bitcoin sales. Strategy's blended acquisition cost sits at approximately $75,700. Any BTC liquidated to fund this transaction would, at current prices, be sold at a gain. The conventional framing that selling Bitcoin signals a change in thesis does not hold up to the arithmetic. Selling an asset at a loss to retire a zero-coupon liability at a discount is a defined financial trade with tax benefits. Whether and at what scale this lever was used remains to be confirmed. The secondary observation is that the option itself matters. A balance sheet that can service a $1.38 billion debt retirement through voluntary asset management - rather than under duress - is a structurally different entity from one that cannot.

Cash. As of May 22, 2026, Strategy held $2.21 billion in cash and cash equivalents. This means cash alone could theoretically absorb the entire $1.38 billion settlement without touching Bitcoin or issuing a single new share. The strategic calculus here is straightforward. A cash-funded redemption carries zero cost of capital, zero dilution, and zero BTC reduction. It extinguishes a fixed liability at a discount to par - the 2029 notes were trading well below face value - and immediately improves the quality of the balance sheet with no market signal required.

The Structural Implications

The debt retirement does two things beyond the immediate balance sheet arithmetic. The first is mNAV breakeven compression. A lower debt load reduces the asset coverage required to sustain the current mNAV premium - the point at which the market's valuation of Strategy's Bitcoin treasury exceeds the liabilities sitting against it narrows. That compression makes future capital raises structurally cheaper.

The second is credit quality. Preferred instruments — STRK, STRF, STRD, STRC — sit above common equity in the capital stack but below senior debt. When the senior debt layer shrinks, the implicit credit support beneath the preferreds improves. A cleaner liability structure strengthens the case for the preferred dividend's sustainability, which in turn supports the instruments' ability to trade near par. For STRC holders and for the ATM programme that depends on par stability, this matters.

The Convertible Transition

Strategy's capital structure has moved through three recognisable phases. The first was convertible debt - zero-coupon instruments that attracted capital through equity optionality at a time when no Bitcoin-native credit market existed. The second was common equity ATM - high-velocity, flexible issuance against a rising mNAV. The third is preferred equity, now a live, trading category generating continuous capital at scale.

The 2029 note repurchase fits within a pattern that has been visible since early 2026: Strategy is retiring convertible debt that has passed its conversion viability threshold while expanding the preferred stack. The notes were useful when MSTR's share price made conversion credible for holders. At $672.40 conversion price against a $183 share price, that window has closed. The debt accrues as a liability without the equity management benefits that justified its issuance.

The convertible market had a ceiling. Saylor acknowledged as much in a recent interview: "We did the converts. We became the biggest issuer of converts in the world... but they all traded cheap. They were all undervalued and we basically maxed out the capital and the market had no more capital. We outgrew the market."

When an instrument trades cheap and the issuer has exhausted the market's capacity for it, retiring that instrument at a discount is a rational reallocation of balance sheet space toward the capital channel that replaced it.

STRC is now an $8.5 billion instrument. The convertible note market served as a bridge to the preferred equity era. Retiring bridge debt once the destination is operational is a logical sequence.

The instinct to treat any Bitcoin liquidation as a negative signal is understandable but analytically incomplete. Strategy's capital structure mechanics define a precise threshold at which selling Bitcoin is accretive.

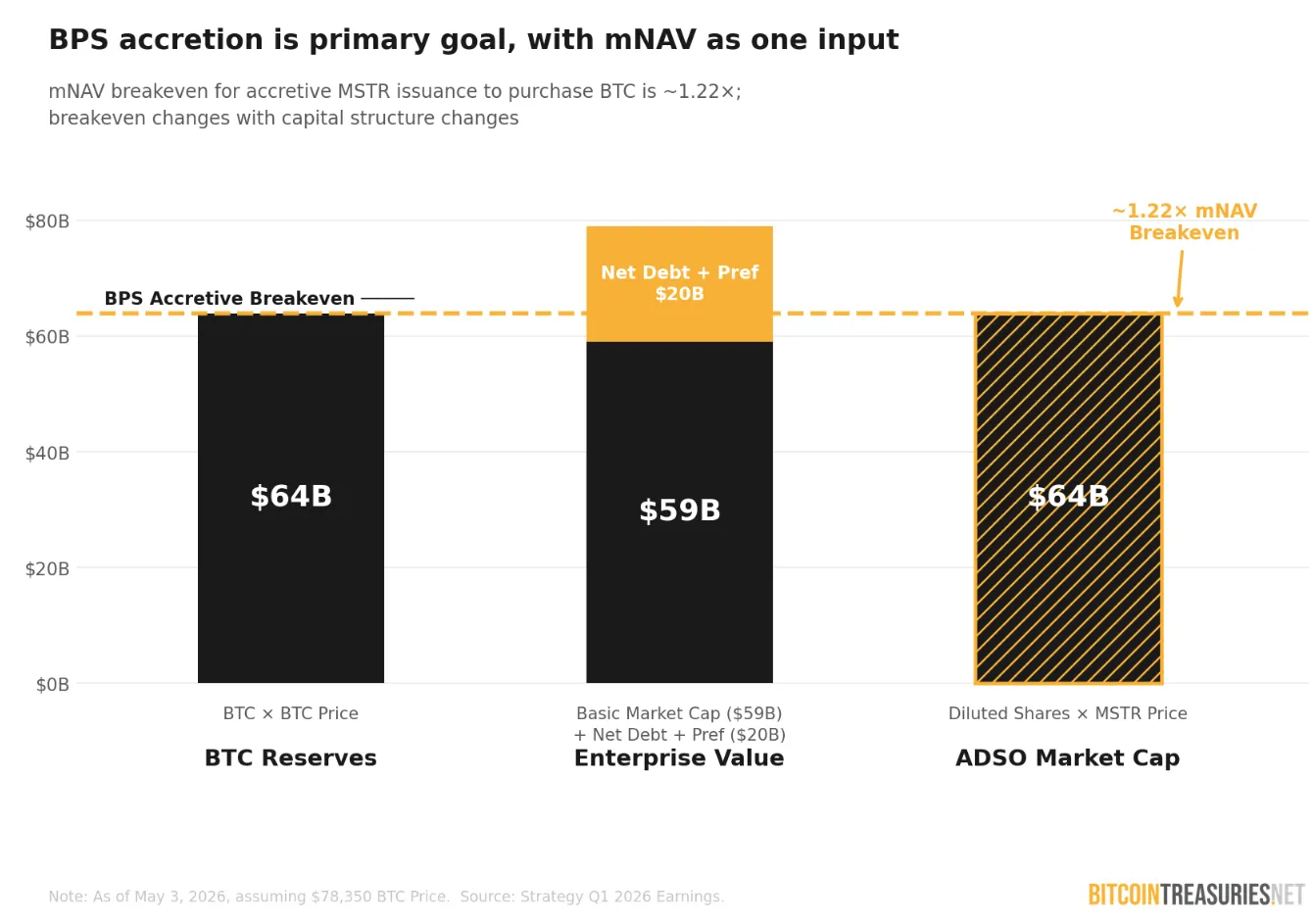

The relevant figure is the mNAV breakeven: approximately 1.22x. Below that level, Strategy's market capitalisation carries insufficient premium to net asset value for ATM equity issuance to be accretive on a per-BTC basis. Issuing shares when mNAV is compressed below 1.22x dilutes existing holders in Bitcoin-per-share terms. At that point, selling Bitcoin directly is the cleaner capital action as no equity dilution occurs, and the liability is serviced at spot. Retiring debt will bring this mNAV breakeven down towards 1x, making BPS accretion more accessible for Strategy.

When Bitcoin is sold to retire convertible notes, the effects compound across the capital structure. The immediate consequence is a reduction in Assumed Diluted Shares Outstanding. The 2029 notes, while out-of-the-money at current conversion prices, still carry a theoretical dilution tail that sits in the ADSO count. Retiring those notes removes that tail entirely, tightening the denominator in the Bitcoin-per-share calculation. Fewer assumed shares outstanding against the same BTC treasury means BPS accretion directly and mechanically without any new Bitcoin needing to be acquired.

The secondary effect is on delta hedging. Convertible notes are hedged by the institutional holders who buy them - typically through short positions in MSTR common stock that track the notes' changing delta as MSTR's share price moves relative to the conversion threshold. Retiring the notes eliminates that hedging pressure. The short interest tied to the convertible arbitrage position unwinds, removing a structural headwind on MSTR's equity price. That dynamic is not widely discussed in coverage of this transaction and is one of the cleaner structural benefits of the repurchase.

The third effect is credit quality. With less senior debt on the balance sheet, the implicit credit support beneath the preferred instruments improves. A reduced senior debt layer narrows the distance between the preferreds and the first-loss position, strengthening the case for dividend sustainability and supporting the instruments' ability to trade near par. Over time, that improved credit profile has implications for how the preferred stack is rated and priced by institutional allocators.

The tax dimension operates separately from all of the above. Strategy's treasury spans years of accumulation across a wide price range. Coins acquired at the higher end of that range carry embedded losses that can be realised on sale. Those recognised losses offset taxable gains elsewhere on the balance sheet. The interaction between tax-loss harvesting on high-cost BTC and discount-to-par retirement of zero-coupon debt creates a liability management window with a tax efficiency component that ATM issuance does not replicate.

The mechanisms are distinct but cumulative. The mNAV threshold governs when Bitcoin sales are more accretive than equity issuance. The ADSO retirement and delta unwind are structural benefits that follow regardless of mNAV. The credit quality improvement accrues to the preferred stack. The tax-loss harvesting governs which Bitcoin to sell - high-cost tranches first, realising losses that reduce the net cash cost of the retirement.

Taken together, this is not a reluctant use of Bitcoin. It is a precise deployment of a capital tool with five separable positive effects on the balance sheet, the share structure, the preferred instruments, and the tax position.

Shrink to Grow

Strategy accumulated 24,869 BTC last week, funded by $2.01 billion in ATM equity sales. The repurchase week and the accumulation week were consecutive, not competing. The balance sheet optimisation and the acquisition programme ran independently, which is the point.

Reducing the debt layer lowers refinancing risk, reduces the mNAV breakeven, and strengthens the credit quality of the preferred stack. Each of those outcomes improves the conditions under which the next capital raise happens. The logic is not complicated: a cleaner balance sheet is a cheaper balance sheet, and a cheaper balance sheet accumulates more Bitcoin over time.

The week without a Bitcoin purchase was not a pause. It was preparation.

Want more bitcoin treasury coverage in your search results? Add Bitcoin Treasuries as a preferred source on Google.