From Bitcoin Accumulation to Bitcoin Credit: The New Financial Hierarchy

On March 30, a filing landed at the SEC that deserved more attention than it received. Strive Asset Management and Tuttle Capital registered the T-Strive Digital Credit ETF - ticker DGCR - an actively managed fund built to hold the preferred stock of Bitcoin treasury companies. Its two core positions: Strategy’s STRC, yielding 11.5%, and Strive’s own SATA, yielding 12.75%. A publicly listed Bitcoin treasury company, building an investable product around the preferred equity of a rival Bitcoin treasury company. Three weeks earlier, Strive had deployed $50 million - over a third of its corporate treasury - into that same STRC instrument.

This is a Bitcoin treasury company subordinating its own capital allocation to the instruments of another. And when you cross that line, you do not cross back. The Bitcoin treasury ecosystem just crossed the Rubicon, with MSTR as its Hegemon.

THE ECOSYSTEM IS REAL

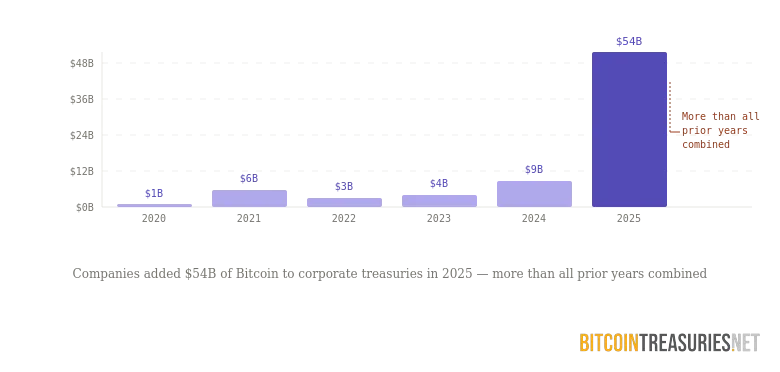

The number of publicly listed companies holding Bitcoin on their balance sheets has surged from roughly 70 at the end of 2024 to 195 today. They added $54 billion of Bitcoin to corporate treasuries in 2025 - more than every prior year combined. The key structural shift occurring now isn’t just the accumulation of Bitcoin - it’s the crossholding of preferred stock.

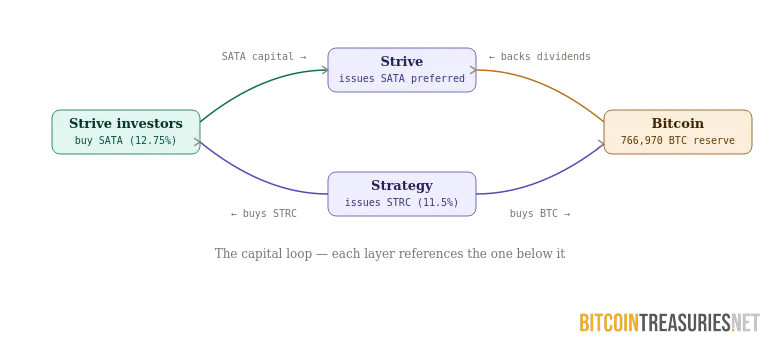

Strive bought $50 million of Strategy’s STRC and booked it as a core balance sheet asset alongside its own 13,741 BTC. CEO Matt Cole stated the company wanted an instrument offering "strong yield dynamics while maintaining stable price behavior with deep liquidity". Then it filed to wrap both STRC and its own SATA preferred stock into an ETF for outside investors. Capital now flows in a loop: Strive’s investors buy SATA, Strive uses that capital to buy Strategy’s STRC, Strategy uses STRC proceeds to buy Bitcoin, and Bitcoin underpins the balance sheets that service the preferred dividends. Each layer references the one below it. This is a financial system in embryo.

What makes this different from 195 companies independently running the same playbook is the emergence of internal capital flows. Strive doesn't just hold Bitcoin - it now holds STRC. DGCR holds the preferred instruments of both. The companies in this ecosystem are no longer just referencing the same asset. They are referencing each other. That is the architecture of a financial hierachy in progress.'

STRATEGY IS THE CENTRE

Every financial system organises around a centre of gravity. In traditional fixed income, that centre is the US Treasury - the instrument so deep, so liquid, and so structurally embedded that every other credit product prices itself in relation to it. The 10-year yield is not just a number. It is the coordinate system of global finance. Everything else is a spread on top of it.

The Bitcoin treasury ecosystem is developing its own coordinate system. And the instrument at its centre is STRC.

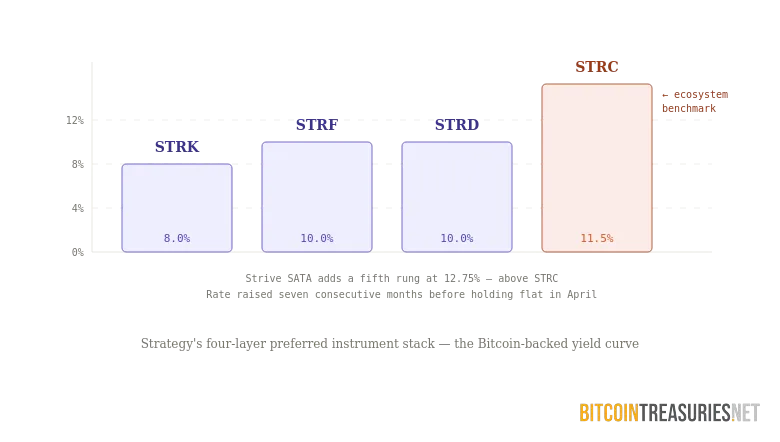

Strategy now holds 766,970 BTC - approximately 3.65% of all Bitcoin that will ever exist - purchased for an aggregate $58 billion. No other entity, public or private, comes close. That position makes Strategy’s equity and preferred instruments the most liquid and widely held Bitcoin-linked securities in the market. When institutions want fixed income exposure to Bitcoin without holding Bitcoin directly, STRC is the first instrument they reach for. Its at-the-market programme still has $22.65 billion in remaining capacity.

Wall Street is noticing. Analysts at Benchmark have described bitcoin-linked fixed income as a potential multi-hundred-billion-dollar market, with Strategy as its architect.

But scale alone does not make a hegemon. What makes Strategy the centre of this ecosystem is the same thing that made US Treasuries the centre of theirs: other participants build on top of it. Strive uses STRC’s yield to service its own preferred obligations. This is putting otherwise idle cash to work. DGCR does not just include STRC as one holding among many. It places STRC at the core of its portfolio construction. When Strive’s Chief Risk Officer Jeff Walton described STRC as offering “clear advantages over traditional fixed income,” he was not comparing it to Treasuries as an alternative. He was positioning it as the benchmark of a parallel system - the instrument against which other Bitcoin-native credit products will be measured.

There is also the matter of intellectual primacy. Saylor did not merely adopt Bitcoin early. He authored the strategic framework - the convertible note raises, the ATM equity programmes, the preferred stock layering, the Bitcoin yield KPI - that every subsequent treasury company has replicated. When Strive issues SATA, it is running the Strategy playbook. When Metaplanet raises capital in Tokyo to accumulate Bitcoin, it is citing the Strategy model. When SWC, Capital B, or any of the 195 companies on the Bitcoin Treasuries leaderboard describe their approach, the intellectual lineage traces back to one source. Imitation in this sector doesn’t weaken the strategy. It validates it. Every new entrant into the Bitcoin treasury space implicitly reinforces Strategy’s position at the apex.

The analogy is precise. US Treasuries did not become the global benchmark because the US government asked nicely. They became the benchmark because the depth of the market, the reliability of the coupon, and the absence of any credible alternative made them the default foundation for everyone else’s capital structure. STRC is following the same path by gravity.

THE ENDGAME

Step back and look at what has been assembled in barely eighteen months. A layered financial architecture: Strategy at the apex, issuing the instruments that define the ecosystem’s benchmark rates. Mid-tier treasury companies like Strive in the middle, subscribing to those instruments while issuing their own. And products like DGCR at the base, packaging it all for traditional capital.

The critics will say it is circular. They are not entirely wrong - but circularity is not a weakness unique to this ecosystem. The entire US dollar system is circular: the government issues debt, the Fed monetises it, banks hold it as reserves. Circularity is not a bug of financial systems. It is a feature. What matters is whether the underlying asset justifies the structure built on top of it.

The question for traditional capital is whether Bitcoin as a treasury reserve asset justifies the emergence of a self-contained capital market with its own credit instruments, its own yield benchmarks, and its own internal hierarchy.

The companies building it have already decided. They’ve crossed the Rubicon.

Want more bitcoin treasury coverage in your search results? Add Bitcoin Treasuries as a preferred source on Google.