Strategy's perpetual preferred remains more than $10 shy of its $100 par value, and the July options chain shows why. Two heavily-populated call strikes and a steadily rising cost to borrow are holding the line just below $90.

The $90 Strike Is Where the Rally Runs Out of Road

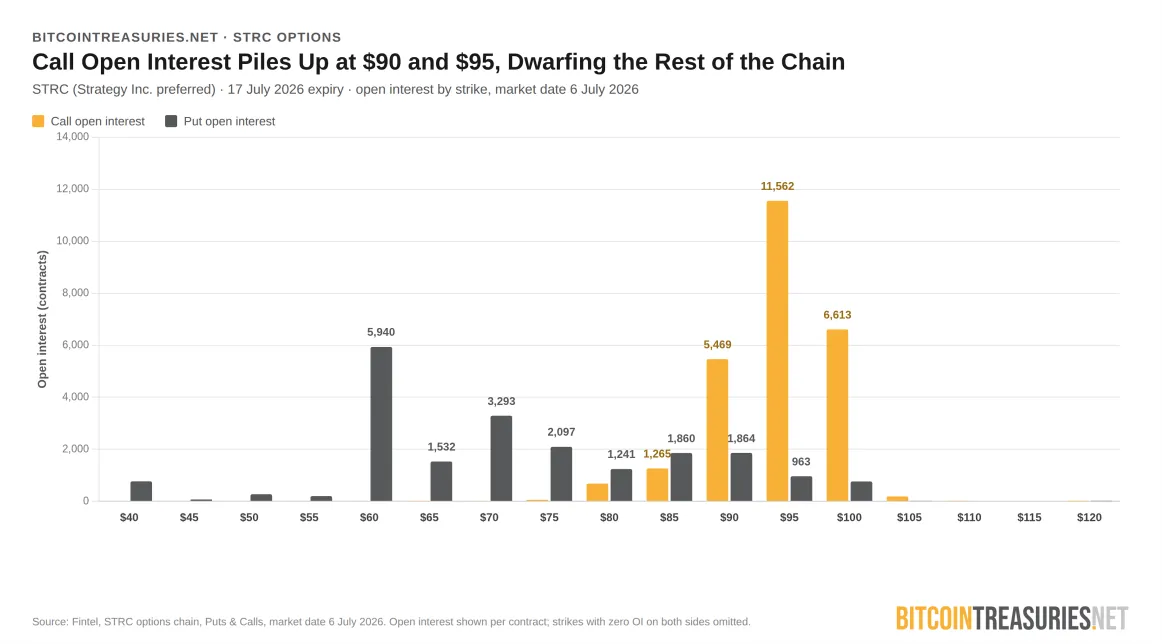

STRC is still trading well below par. The July 17 options chain explains the immediate friction. At the $90 strike, open interest - the number of contracts currently outstanding, a proxy for how much capital has a stake at that price - stands at 5,469 call contracts. The delta on those calls, which measures how much the option's price moves for every $1 move in STRC and doubles as a rough probability the contract expires in the money, sits at 0.48. That is almost exactly at the money: the stock is close enough to the strike that dealers holding the other side of those contracts must trade in and out of STRC continuously just to stay hedged as it moves. The put side confirms the same picture: 1,864 contracts of open interest at $90, with a delta of -0.54 (puts carry a negative delta because they gain value as the stock falls). Between them, the two books describe a preferred pinned right at the boundary, not through one strike's mechanics but through both.

The Real Wall Sits at $95, Not $90

The bigger obstacle isn't at $90 - it's above it. The $95 calls carry 11,562 contracts of open interest, more than double the $90 strike. Volume - the number of contracts that actually changed hands that day, as opposed to open interest's running total - hit 1,727 on 6 July alone, which shows the position being actively built rather than sitting stale on the book. Weighting each strike's open interest by its per-contract gamma gives a rough measure of dealer hedging exposure. Gamma measures how fast delta itself accelerates as the stock approaches a strike; the higher it runs, the more aggressively dealers have to buy or sell the stock to stay hedged. At 0.06 gamma and 5,469 contracts, the $90 strike works out to roughly 328 units of hedging load; at 0.05 gamma and 11,562 contracts, $95 works out to roughly 578. On that measure, $95 represents nearly twice the hedging load of $90 despite sitting five dollars further from the tape.

If the writers of those $95 calls are net short the position - meaning they sold the calls and don't hold enough STRC to offset that exposure, the standard read for a concentration of this size - market makers hedging that book would need to sell into any rally that approaches the strike. That's the mechanical root of a "pinning" effect: hedging flow that pushes back against the stock right as it nears the strike, capping the move. That assumption can't be confirmed from open interest alone; the chain shows contracts outstanding, not which side holds them.

Borrow Costs Are Climbing, Just Not in a Straight Line

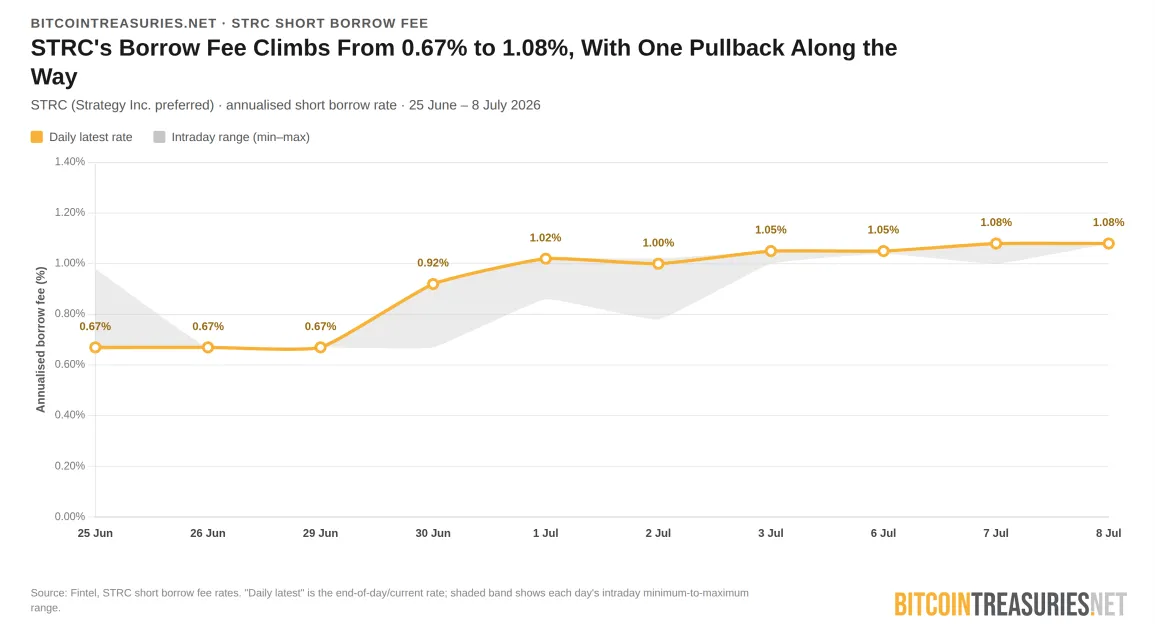

STRC's borrow fee - the annualised rate a trader pays to borrow STRC shares in order to sell them short - remains cheap in absolute terms. At 1.08%, it sits well inside the range brokers treat as general collateral, nowhere near what counts as genuinely hard to borrow. That's arguably a bigger obstacle to a run at par than an expensive fee would be. A high, rising borrow cost usually signals scarcity: shares are hard to find, and short sellers face real pressure to cover if the stock turns, which is the classic setup for a squeeze that forces price higher. A cheap fee means the opposite. Shares to borrow are freely available, so short sellers and the market makers running the option hedges described above can lean on STRC, or add to positions near $90 and $95, without paying much for the privilege. There's no supply-side pressure building underneath that could force a short-covering rally and help clear the wall.

The fee has still moved, and the direction is consistent with the options picture. It held flat at 0.67% through late June, then climbed through early July: 0.92% on 30 June, 1.02% on 1 July, a slip to 1.00% on 2 July (touching as low as 0.78% intraday that session), before resuming to 1.05% on 3 July, flat through 6 July, and 1.08% by 7–8 July - a rise of 0.41 percentage points, or roughly 61% in relative terms, over two weeks. However, building from a base low enough that shorting STRC still costs next to nothing.

The Wall Has an Expiry Date

Every figure in this chain is tied to the 17 July contracts. Once those expire, the specific open interest sitting at $90 and $95 clears off the board. Whether that unlocks a cleaner run at par, or the next monthly chain simply rebuilds the same overhead at similar strikes, is the open question. Until then, STRC's path back to $100 runs directly through a market structure that is working against it.

Want more bitcoin treasury coverage in your search results? Add Bitcoin Treasuries as a preferred source on Google.