Why Metaplanet Should Buy Nakamoto to Issue US Bitcoin Preferred Stock

Strive's CEO sketched a deal between Metaplanet and Nakamoto on a recent podcast. He has no insider knowledge. The idea is worth examining anyway, because it answers a question each company is currently failing to answer alone.

Matt Cole was asked when mergers make sense in the Bitcoin treasury sector. He ruled out Strive buying again. Then he offered an example involving two companies he does not run.

What if Metaplanet bought Nakamoto, and Nakamoto then issued US preferred stock?

Cole was careful. He said he had no insider information about any deal. He framed it as a scenario, not a forecast. But the scenario is precise, and it lands on the exact constraint each company is fighting. That is what makes it worth taking seriously.

Metaplanet wants to issue a US-style perpetual preferred. It cannot right now at adequate speed. Nakamoto has a US listing and almost nothing to do with it. Cole's idea puts the two facts in the same sentence.

Nakamoto is a listing in search of a balance sheet

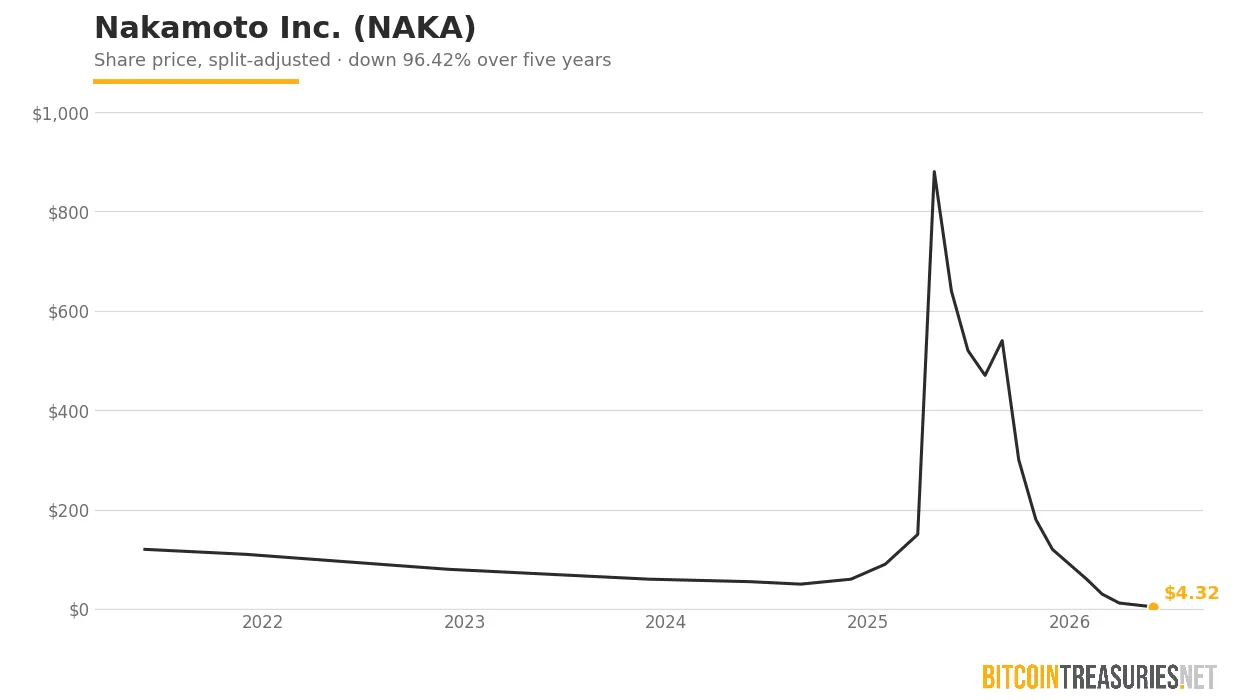

Nakamoto holds 5,058 Bitcoin. That stack is worth roughly $370 million. The company's market capitalisation is around $75 million. The equity trades at a deep discount to the Bitcoin behind it.

The share price tells the rest. Nakamoto is down roughly 99% from its 2025 high. To stay on the Nasdaq it executed a 1-for-40 reverse split in May, collapsing about 696 million shares into roughly 17 million. The split bought time but hasn't repaired the price.

The company got here by spending its credibility. In March it sold 284 Bitcoin, around $20 million, to cover working capital and costs tied to acquisitions. Those acquisitions were BTC Inc. and UTXO Management, two firms founded by CEO David Bailey, bought in a $107.3 million all-stock deal that diluted public holders. Bailey sat on both sides of the transaction.

The pay told the same story. Nakamoto's first-quarter 10-Q showed compensation expense of $7.3 million, up sevenfold from $1.0 million a year earlier, against $2.3 million of operating revenue and a $238 million net loss. Bailey's own compensation runs through consultancies he controls. So the picture handed to shareholders was a stock down 99%, a forced Bitcoin sale, related-party acquisitions that doubled the share count, and a compensation line rising while the equity collapsed. A chief medical officer left over from the KindlyMD reverse merger, kept on to satisfy a Nasdaq operating requirement, became the punchline.

What Nakamoto still owns is the thing Metaplanet cannot manufacture. A Nasdaq listing. A US issuer with a public vehicle attached.

Metaplanet is an issuer with nowhere to issue

Metaplanet has the opposite problem. It holds 40,177 Bitcoin, the third-largest corporate stack in the world. It has scale, a clean structure, and a strong shareholder base. What it does not have is a working preferred instrument.

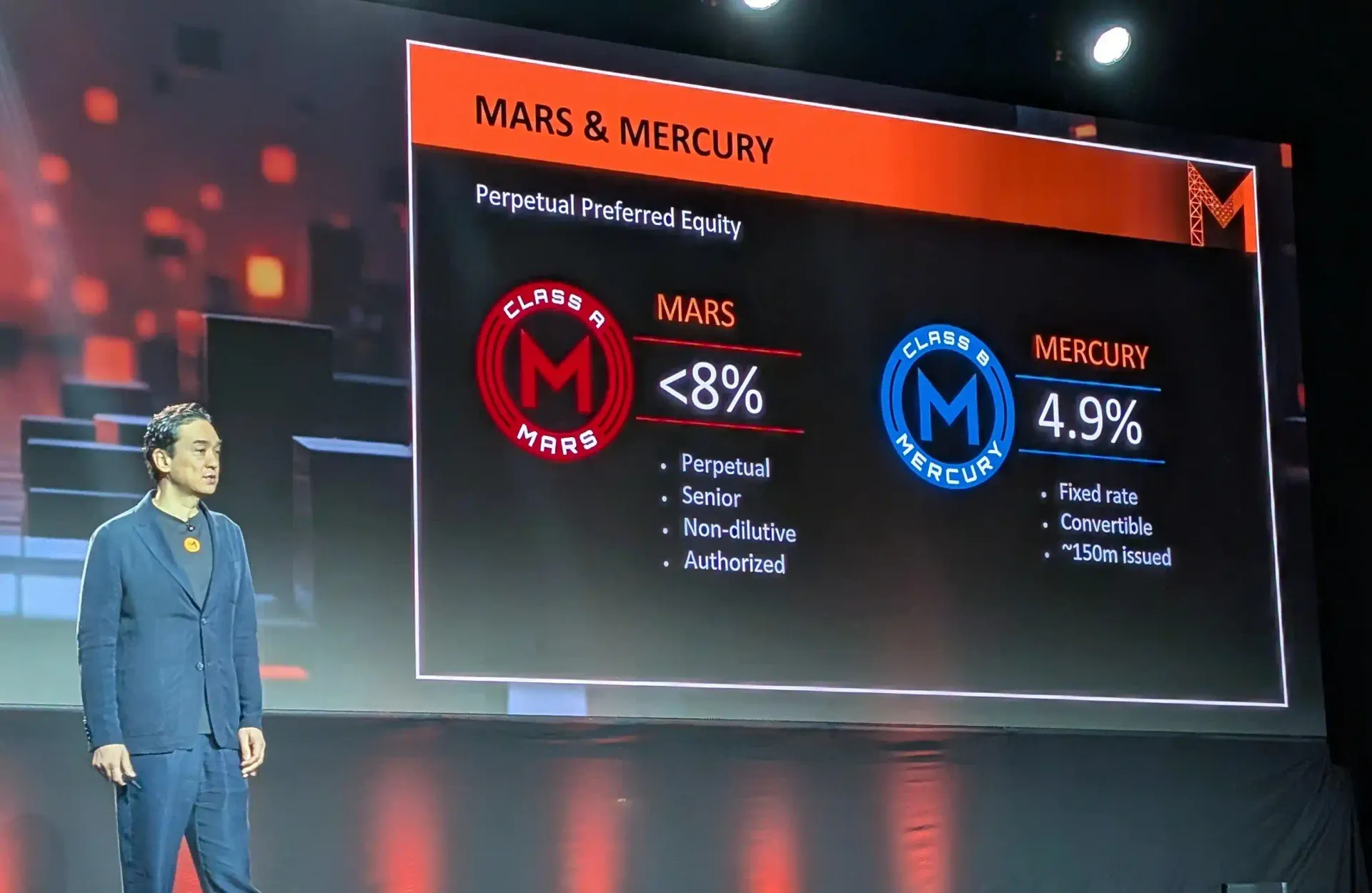

The plan was MARS and MERCURY. MARS is the STRC analogue, a monthly adjustable-rate preferred. MERCURY sits a tier below. On 13 May, CEO Simon Gerovich announced that these were to be delayed.

He named the reasons. Japanese exchange rules require preferred dividends to be backed by sustainable, recurring cash flow tested across market conditions. Metaplanet has a six-quarter operating record to point to. The instrument would be only the sixth or seventh listed preferred in Japan, and the first perpetual. Monthly dividends, standard for STRC, are alien to a market that pays once or twice a year.

The cost of the delay is visible in the stock. Metaplanet trades near its lowest level since late 2024, down around 41% this year, underperforming Bitcoin, Strategy and Strive. A $725 million impairment in the first quarter did not help. Shareholders who bought the Strategy-of-Japan thesis are waiting on an instrument that Japan's market structure may not permit for a long time.

So Metaplanet wants to issue in the US. Cole's framing of the obstacle was exact. Metaplanet has no US operating company, no listed US vehicle, and no established issuer status in the United States.

The case for

The deal solves both constraints at once. Metaplanet absorbs a US-listed entity and inherits, in effect, a Nasdaq platform from which a familiar STRC-style preferred could be issued to American capital. The blocked instrument finds a market. Bailey already advises Metaplanet, and Nakamoto and UTXO have both invested in it, so the two are not strangers.

For Nakamoto holders, a merger at any reasonable mark would re-rate a stock that the market has left for dead. A discounted vehicle folded into a 40,177-Bitcoin balance sheet is a different security. Cole's read was that sentiment toward Nakamoto would improve sharply.

There is also a cheaper-Bitcoin angle. Buying a company trading below the value of its Bitcoin is a way to add coins at a discount to spot. That is the logic that drew Strive to Semler Scientific, whose 5,048 Bitcoin came attached to preferred-share ambitions of Strive's own.

The case against

The obstacles are not small, and Cole did not pretend they were. The two companies sit in different countries. A cross-border combination raises tax, regulatory and structural questions that a domestic deal does not. Cole himself was unsure it could be done cleanly.

Then there are Nakamoto's operating businesses. Strive is unwinding Semler's healthcare arm. Nakamoto's equivalents, BTC Inc. and UTXO, were bought by Bailey from Bailey. Stripping them back out is unlikely to be something he wants, which complicates any clean treasury-for-listing swap.

The hardest problem is trust. Nakamoto spent its reputation on a Bitcoin sale, a near-total drawdown, related-party acquisitions funded by dilution, and a pay structure that grew as holders were wiped out. A merger does not erase that history. Metaplanet would be importing a damaged brand into its own shareholder base at a moment when its own holders are already restless.

What would have to be true

Cole's own verdict was a shrug, and an honest one. He did not know whether it made sense for both sides. He could imagine scenarios where it did.

That is the right place to leave it. There is no evidence a deal is being discussed. What there is, is a structural fit. One company has a listing and no use for it. The other has a use and no listing. For the idea to move from a podcast to a term sheet, the cross-border mechanics would need to clear, Bailey would need to accept a diminished role, and Metaplanet would need to decide that a US preferred is worth inheriting Nakamoto's past to get it.

Want more bitcoin treasury coverage in your search results? Add Bitcoin Treasuries as a preferred source on Google.