The case for STRC is intact. The case for holding the dividend at 11.5% is no longer.

The product works. The mechanism has a blind spot.

STRC is a transformative financial instrument. A variable-rate perpetual preferred, reset monthly against a VWAP target, designed to hold par across Bitcoin's volatility while funding the most aggressive institutional Bitcoin accumulation programme ever attempted - that is impressive financial engineering. It has worked. Since launch in July 2025 at a 9% coupon, the board has raised the dividend seven times in response to market feedback. The framework was built to be responsive. The problem is the frequency, not the principle.

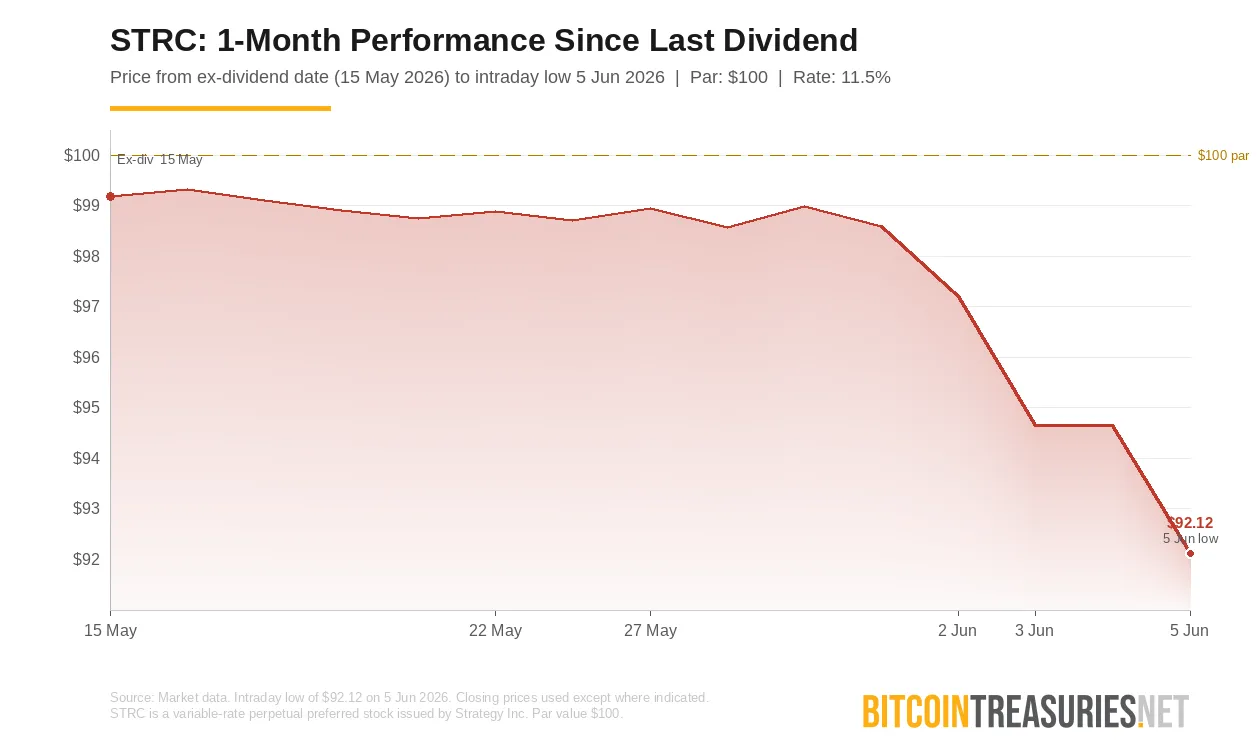

Today STRC hit an intraday low of $92.12. Despite the fact it is not a reason to panic about the product, it is a quantifiable reason to raise the rate.

The yield maths have moved beyond a single reset

At $100 par, an 11.5% coupon produces $11.50 annually. At today's intraday low of $92.12, that same $11.50 implies a current yield of 12.49% - nearly 100 basis points above the stated coupon. The market is not sending a subtle signal. It is demanding a yield that the current rate cannot deliver at par and expressing that demand through price.

The framework's own sub-$95 trigger prescribes a minimum 50 bps increase. That takes the coupon to 12.0%. At 12.0%, STRC re-anchors to par only if the market's required yield simultaneously falls back to 12.0%. At a $92.12 print, a single 50 bps reset does not close the gap. The board should treat the framework minimum as a floor, not a target. A rate at or above 12.5% is what the current dislocation is asking for.

Why the framework misfired this month

The mechanics are straightforward. The full-month VWAP for May came in at $99.62, keeping shares close enough to their $100 par value to sit within the $95-$101 target band. No adjustment warranted. The framework read last month's temperature and found it acceptable. Bitcoin's move lower came on June 2-3, after the reset window had already closed.

This is a design feature, not a design flaw - but it has a consequence. In a fast drawdown, STRC is structurally undefended for up to a month. The thermostat cannot respond until the end of June at the earliest. Meanwhile the price gap compounds. What was a 65 basis point dislocation on June 3 is now approaching 100 basis points. Each day the rate sits at 11.5%, the distance the July reset needs to close grows wider.

The semi-monthly vote is good. It is not enough on its own.

The June 8 shareholder vote proposes moving STRC dividends from monthly to semi-monthly - the same annualised rate, paid twice as often. This is worth passing. Smaller, more frequent payments reduce the cyclical ex-div dip, create more entry and exit windows, and dampen per-payment volatility. But frequency and adequacy are separate dimensions. Receiving 11.5% in 24 instalments rather than 12 does not change the yield. The market is not discounting STRC because payments arrive monthly. It is discounting STRC because 11.5% is insufficient for current conditions.

The semi-monthly proposal will increase stability but only at a favourable market rate. A $92.12 print is a rate problem.

Competition is applying pressure from within Strategy's own stack

SATA launched at 13% with daily dividend payments, moving to that cadence on June 16. STRC at 11.5% yields less than SATA and soon to be less payments with daily dividends for SATA. For a capital allocator seeking yield, that positioning is difficult to defend at a near 8% discount to par when SATA is available from a comparable issuer at a higher rate. Raising STRC to at least 12% restores the instrument's relative-value logic and re-establishes the yield gap that justified its positioning.

The verdict

STRC is a transformative product with established proof of work. However, it is operating in a stressed market environment. The Bitcoin thesis is intact, the treasury is substantial, and the instrument's core mechanics remain sound. None of that is in dispute here. What is in dispute is whether the board uses the July reset to meet the market where it is or holds at a minimum that was calibrated for a different environment.

At $92.12, the market's answer is unambiguous. It is demanding 12.49%. The board should respond in kind - not with the framework minimum of 50 bps, but with a rate that reflects the current clearing yield. A reset to minimum 12% at the next declaration, combined with Bitcoin stabilisation and the semi-monthly structure coming online, is the combination that re-anchors STRC to par durably. The product deserves that fix. So do its holders.

12% should be the floor.

All opinions are held by the writer and not BitcoinTreasuries.net.

Want more bitcoin treasury coverage in your search results? Add Bitcoin Treasuries as a preferred source on Google.