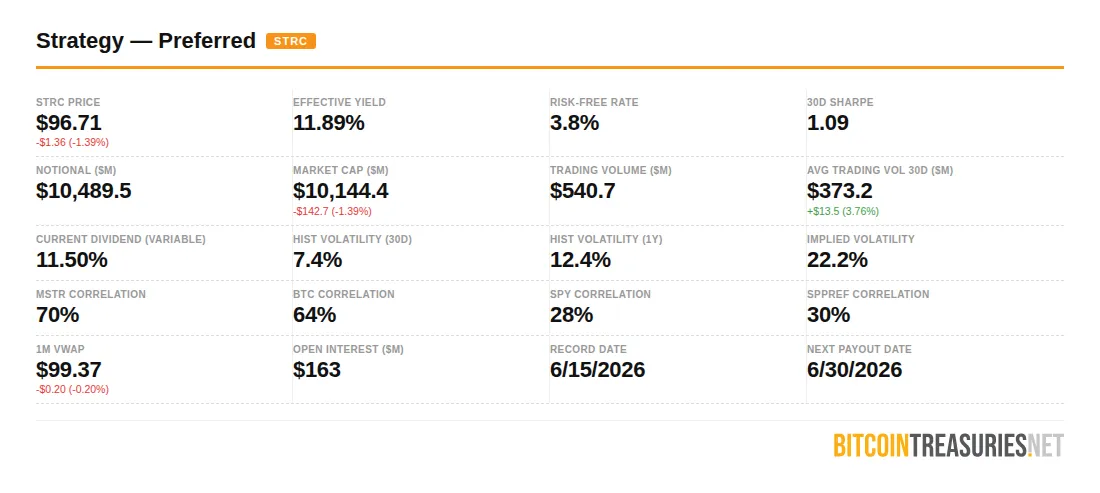

With Bitcoin at $67,207 and STRC already trading at $96.71, slightly below its $100 par value, a number of holders of Strategy's preferred stock are quietly running the same stress test. Not "when does this get uncomfortable?" but "at what price does this actually break?"

It's a fair question. And the answer depends almost entirely on one variable: what you believe Bitcoin does from here.

Michael Saylor framed it as cleanly as anyone has. "If you think Bitcoin is going to zero tomorrow forever, you don't want to own this. If you actually believe in Bitcoin, it's not terribly risky." He went further: "If you think Bitcoin is as good as the S&P, this is investment grade. If you think Bitcoin outperforms the S&P, it's almost riskless. If you think Bitcoin goes to zero, then this is distressed credit."

That is an unusually honest product description. It is also a useful analytical framework, because the answer to "can STRC blow up" is less a question of product design and more a question of Bitcoin's long-term trajectory. For believers, the current dip to $96.71 is a buying opportunity with an 11.89% effective yield. For skeptics, the structural risks below are worth understanding before sizing a position.

First, a Note on Strategy's 32 BTC Sale

A few days ago, Strategy disclosed the sale of 32 Bitcoin. Predictably, corners of crypto Twitter treated it as a distress signal, the beginning of the end, the first crack in the dam.

It almost certainly wasn't.

Selling 32 BTC when you hold 843,706 is not a liquidity event. It's a rounding error. The more plausible read is that this was deliberate market education. Strategy was signaling to institutional holders and analysts that Bitcoin sales are a normal operational tool, not an emergency lever. You don't panic-sell 32 coins. You teach the market what a controlled sale looks like before you ever need to do a large one.

Saylor addressed the concern directly: "Even if we sell 1 Bitcoin, we will buy 10x-20x more. It should be a non-issue after people understand it." He also laid out the math that makes that statement more than just confidence: "If we issue STRC equal to 2.3% of our Bitcoin holdings, we will be a net buyer of BTC forever, even if we sell BTC to pay the dividend." That is the structural logic that turns a dividend obligation from a liability into an accumulation engine. The preferred program is not competing with Bitcoin buying. It is funding it.

The scale of that accumulation is worth sitting with for a moment. Saylor recently noted that Strategy has already bought $11 billion of Bitcoin so far this year, purchasing at 2x the rate miners are able to produce it. The STRC preferred program alone is running at a $24 billion annual rate, which Saylor says will buy 2x to 3x the entire Bitcoin supply produced by miners on its own. That is not the capital deployment profile of a company preparing to sell. It is the profile of a company that views every dip as a reloading opportunity.

Not all Bitcoin sales by Strategy are net negatives for MSTR holders either. Tax-loss harvesting is one obvious mechanism, selling depreciated BTC at a loss to offset gains elsewhere in the corporate structure while maintaining effective exposure through reinvestment. Another is NAV reset management: selling Bitcoin at a calculated moment allows Strategy to reset its cost basis, potentially improving future reported return metrics and giving management flexibility to re-enter at lower prices, which is accretive if Bitcoin subsequently recovers. The 32-coin sale may serve one or both of these purposes. A sale is not automatically bearish on the company's Bitcoin conviction.

The Capital Structure Almost Nobody Reads

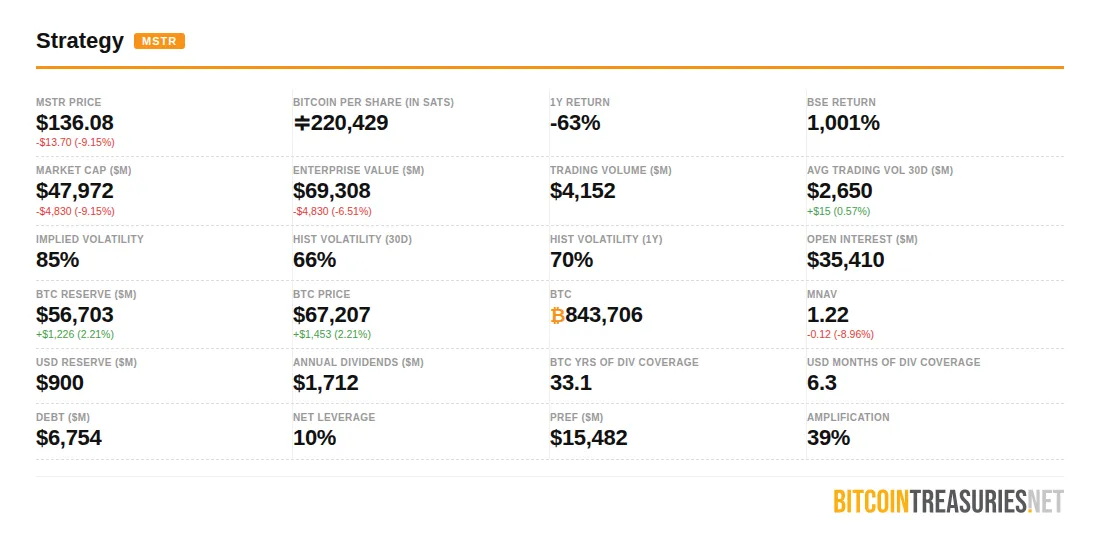

STRC is a preferred stock. It's worth understanding where it sits in a hypothetical Strategy liquidation scenario. In any wind-down scenario, convertible debt holders, currently $6.754 billion per Strategy's own dashboard, get paid before STRC and the other preferred classes. The total preferred obligation across all classes sits at $15.482 billion. Common shareholders (MSTR) are last.

The important thing to understand here is that STRC is actually well protected relative to MSTR common stock. It sits significantly higher in the waterfall. Common equity gets zeroed out first and gets zeroed out hard. STRC holders have a much larger buffer before they see any real impairment.

At Bitcoin's current price of $67,207, Strategy's 843,706 BTC is worth $56.7 billion. BTC value divided by senior claims: $56.7B / ($6.754B + $15.482B) ≈ 2.5x coverage. The BTC reserve alone covers annual dividend obligations at a ratio of 33.1 years. That is not the balance sheet of a company approaching distress.

The bear case math does compress on the way down, it's true. At approximately $26,290 per Bitcoin, MSTR common equity is wiped out entirely. But that number is roughly 60% below current prices. STRC has a long runway before reaching genuine impairment territory, and the yield adjusting upward automatically as price falls means holders are compensated for the incremental risk in real time.

The Number That Actually Matters: Around $50,000

The STRC product is designed with meaningful downside protection. The $100 par value creates a redemption floor. Right now STRC is at $96.71 with an effective yield of 11.89%, already reflecting some risk premium above the stated 11.5% target. At $95 that yield would push toward 12%, which historically stabilizes demand for income products. There are no margin calls or forced redemptions in the traditional sense, and Strategy carries 6.3 months of USD cash coverage at current annual dividend obligations of $1.712 billion covered by a $900M USD reserve.

The bull case here is straightforward. If Bitcoin climbs from $67,207 toward the $200,000 to $500,000 range that a number of credible analysts including Saylor himself have projected, the collateral base expands dramatically. Strategy's $56.7 billion BTC reserve becomes $150 billion or more. The preferred stack that represents $15.482 billion against $56.7 billion in collateral today becomes a tiny fraction of the total asset base. STRC at $96.71 with an 11.89% yield, bought today, would look extraordinarily cheap in retrospect. And with STRC's $24 billion run rate absorbing 2x to 3x annual miner supply, the structural demand pressure on Bitcoin's price is not easing. It is compounding.

The stress scenario requires a prolonged bear market below $50,000 sustained over multiple quarters, not a brief dip. At that level, Strategy's mNAV, currently 1.22, could approach 1.0, which constrains the ability to issue new common shares accretively. New preferred issuance would also get harder. The $1.712 billion annual dividend obligation would lean more heavily on the $900 million USD reserve and on Bitcoin sales to bridge any gap. That is a tighter operating environment, though not a catastrophic one given the depth of the BTC collateral at any price above $30,000. And even in that scenario, Saylor's 2.3% issuance threshold math suggests the company can sell Bitcoin to fund dividends and still remain a net accumulator, provided issuance stays within that boundary.

The Reflexive Dynamic Cuts Both Ways

The scenario bears discuss most is Strategy getting caught in a reflexive selling loop. If the company approached distress and began selling large quantities of its 843,706 Bitcoin, that selling pressure could push Bitcoin lower, worsen the balance sheet, and force more selling.

What gets less attention is that the reflexive dynamic works just as powerfully in the other direction. Strategy's 39% amplification factor, visible on the dashboard today, means that a sustained Bitcoin rally compresses the preferred obligations as a percentage of assets rapidly. A move from $67,207 to $100,000 per Bitcoin would add roughly $27.7 billion to Strategy's BTC reserve. The preferred stack stays fixed at $15.482 billion while the collateral base grows dramatically. STRC's risk profile improves nonlinearly on the way up.

Today's 9.15% single-day drop in MSTR to $136.08 illustrates the leverage in both directions. The same amplification that stings on a down day supercharges returns when Bitcoin trends higher for months. Holders who bought STRC during previous dips below par have collected double-digit yields while the collateral base recovered. And with Strategy already buying Bitcoin at 2x miner production rates this year and Saylor on record saying any Bitcoin sold will be replaced at 10x to 20x the volume, the institutional intent behind the treasury strategy has not quietly shifted. The accumulation playbook remains intact.

Putting It Together

The honest answer to "can STRC blow up" is: yes, under a specific set of conditions that require Bitcoin to fall roughly 26% from current levels and stay there for an extended period while Strategy simultaneously loses access to capital markets. That is not a scenario to dismiss entirely, but it is also not the base case for anyone with meaningful Bitcoin conviction.

Saylor's own framework remains the cleanest guide. If you believe Bitcoin outperforms the S&P over the next decade, STRC at $96.71 yielding 11.89% is, as he said, almost riskless. If you believe Bitcoin roughly matches broad equity returns, it is investment grade income with Bitcoin upside on the collateral. The only scenario where STRC genuinely fails is the scenario where Bitcoin fails, and if you believe that, the product was never designed for you.

At $67,207 today with STRC at a $3.29 discount to par, an effective yield approaching 12%, a company buying Bitcoin at twice the rate miners produce it, and a structural design that keeps Strategy a net Bitcoin buyer even when selling to fund dividends, the market is offering a modest entry premium for the risk. For holders with a multi-year Bitcoin outlook, that premium looks reasonable. For holders who need to know their $100 is safe next quarter regardless of what Bitcoin does, there are better products for that job.

All figures sourced from Strategy and STRC dashboards as of June 3, 2026.

Want more bitcoin treasury coverage in your search results? Add Bitcoin Treasuries as a preferred source on Google.