Sweden's BTC Treasury Capital Wins The Race to Europe's First Bitcoin Preferred

On Monday a fixed-dividend preferred share backed by Bitcoin starts trading on Stockholm's Spotlight market. It is the first of its kind to reach a European venue, and it arrives from a treasury of fewer than 200 coins while the larger issuers circling the same structure in Britain and France are still assembling the machinery to follow.

On Monday 20 July, BTC PREF begins trading on the Spotlight Stock Market in Stockholm. B Treasury Capital AB - Bitcoin Treasury Capital, listed under BTC B for its ordinary shares - will by then have carried a Bitcoin-backed preferred all the way to a public order book before any other European treasury company. Pareto Securities steps in as liquidity provider from the first day of trading.

The scale contrast is the part worth pausing over. France's Capital B holds 3,139 BTC. The Smarter Web Company holds around 2,878. H100, the Nordics' largest treasury, holds roughly 1,051 and is acquiring its way toward 3,500. BTC AB's treasury sits some way below any of them. Every one of these companies has talked about a preferred or credit instrument; the one that reached the tape first did so from the smallest balance sheet of the four, under founder-CEO Christoffer De Geer, at a company that listed its ordinary shares only in July 2025. On this evidence, getting there first was a matter of execution rather than size.

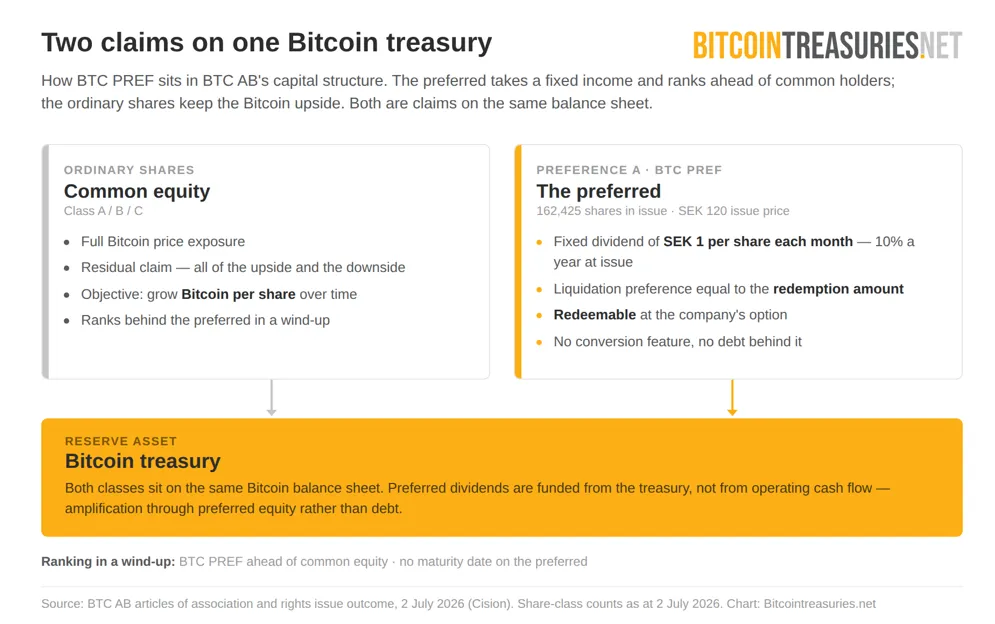

A fixed claim on the treasury, callable at the company's option

BTC PREF is a preference A share priced at SEK 120.00. It pays a fixed dividend of SEK 1 per share each month, which is 10 per cent a year at the issue price. It carries a liquidation preference equal to its redemption amount and can be redeemed by the company under the terms set out in the articles of association and the information document. There is no conversion feature and no debt sitting behind it.

The company's own framing is amplification without leverage. In the June resolution BTC AB described the structure as a way to raise equity capital without creating debt or large repayment obligations, and to "prudently increase its amplification through preferred equity" with the objective of growing Bitcoin per share while limiting dilution for ordinary holders. De Geer put the mechanics more plainly at an investor-day Q&A last October: the company takes Bitcoin's volatility and packages it into a flat monthly dividend, keeping the spread, while common holders carry "the risk of the ups and downs". He described the regulatory path as equally straightforward, calling BTC AB "just an investment company" and therefore outside MiCA. That is the STRC logic rendered in Swedish corporate form: a fixed claim funded from a Bitcoin balance sheet rather than from operating cash flow.

One qualifier belongs in the reader's mind from the start. Spotlight is a multilateral trading facility, not a MiFID II regulated market. The instrument is listed in the loose sense of admitted to trading, not in the sense a main-board issue would be.

The rights issue was set at a maximum of 195,078 preference shares. Existing Class B holders could subscribe for one BTC PREF for every four subscription rights. When the book closed on 30 June, 29,192 shares had been taken up on rights and a further 72,833 without, a total of 52.3 per cent. The issue raised gross proceeds of about SEK 12.2 million and net proceeds of about SEK 11.9 million against a fully subscribed target near SEK 23.4 million. The preferred count rose from 60,400 to 162,425.

This was the second outing for the instrument, not its debut. BTC AB placed 60,400 of the same preference shares privately in December 2025, raising SEK 7.2 million from institutional and professional investors. The rights issue is the first public-facing version of that class. A book that clears at just over half, in a market that has spent the first half of 2026 well below last October's highs, is a measured verdict. The real read comes at the open on Monday, when secondary demand meets a fixed 10 per cent coupon.

Britain cleared the runway last week

The reason this is a European story and not only a Swedish one is that two larger issuers moved within the same fortnight.

The Smarter Web Company reached the decisive stage first. On 14 July the High Court of Justice in England and Wales confirmed the company's £210 million capital reduction, cancelling that sum from the share premium account and moving it into distributable reserves. The court order was delivered to the Registrar the following day and takes effect on registration. The reduction returns no capital and leaves the issued share count of 371,965,705 ordinary shares untouched. What it does is create the reserves a sterling Bitcoin preferred would be paid from. CEO Andrew Webley has signalled the instrument could arrive before the fourth quarter, sitting on a treasury of 2,878 BTC. The enabling step is now behind it; the instrument is the next thing the market is waiting on.

France has the mandate, not yet the instrument

Capital B holds the broadest authorisation and the least finished product. At its 17 June meeting in Puteaux, shareholders approved, with more than 95 per cent support, a framework of up to €5 billion in equity issuance and up to €100 billion in credit instruments. Executive Alexandre Laizet used an appearance at BTC Prague to sketch a digital credit instrument for European investors, tracing the STRC and SATA framework, targeting double-digit yields with volatility held below double digits, and citing a tenfold rise in demand for such products year on year. Capital B sits on 3,139 BTC, among the largest treasuries in Europe. It has the balance sheet and the mandate. It does not yet have a listed instrument.

The template now exists, and it travels

Set the three side by side and the sequence is instructive. The company with the mandate has no instrument. The company that cleared the legal runway has no instrument yet either. The company with the smallest treasury has the only one trading. For all the attention on the larger names, the reference transaction for a European Bitcoin-backed preferred is now Swedish, and it did not take a large balance sheet to get there.

That is the point that carries forward. The structural logic - fixed-dividend preferred equity, funded from a Bitcoin treasury, engineered to lift Bitcoin per share without diluting common holders - does not require a large balance sheet to attempt. It requires distributable reserves, a willing venue and an appetite for a fixed coupon. Britain's smaller listed treasuries have watched Smarter Web clear the capital-reduction path and will have taken the note. H100, whose stated strategy is explicitly to grow Bitcoin per share "through innovative financial instruments" is an obvious candidate to formalise the same idea in the Nordics. None of them has announced a preferred. Yet.

Whoever lists the next European Bitcoin preferred, and whatever its size, they will be issuing into a market where the instrument already has a live European precedent. That precedent trades from Monday.

Want more bitcoin treasury coverage in your search results? Add Bitcoin Treasuries as a preferred source on Google.