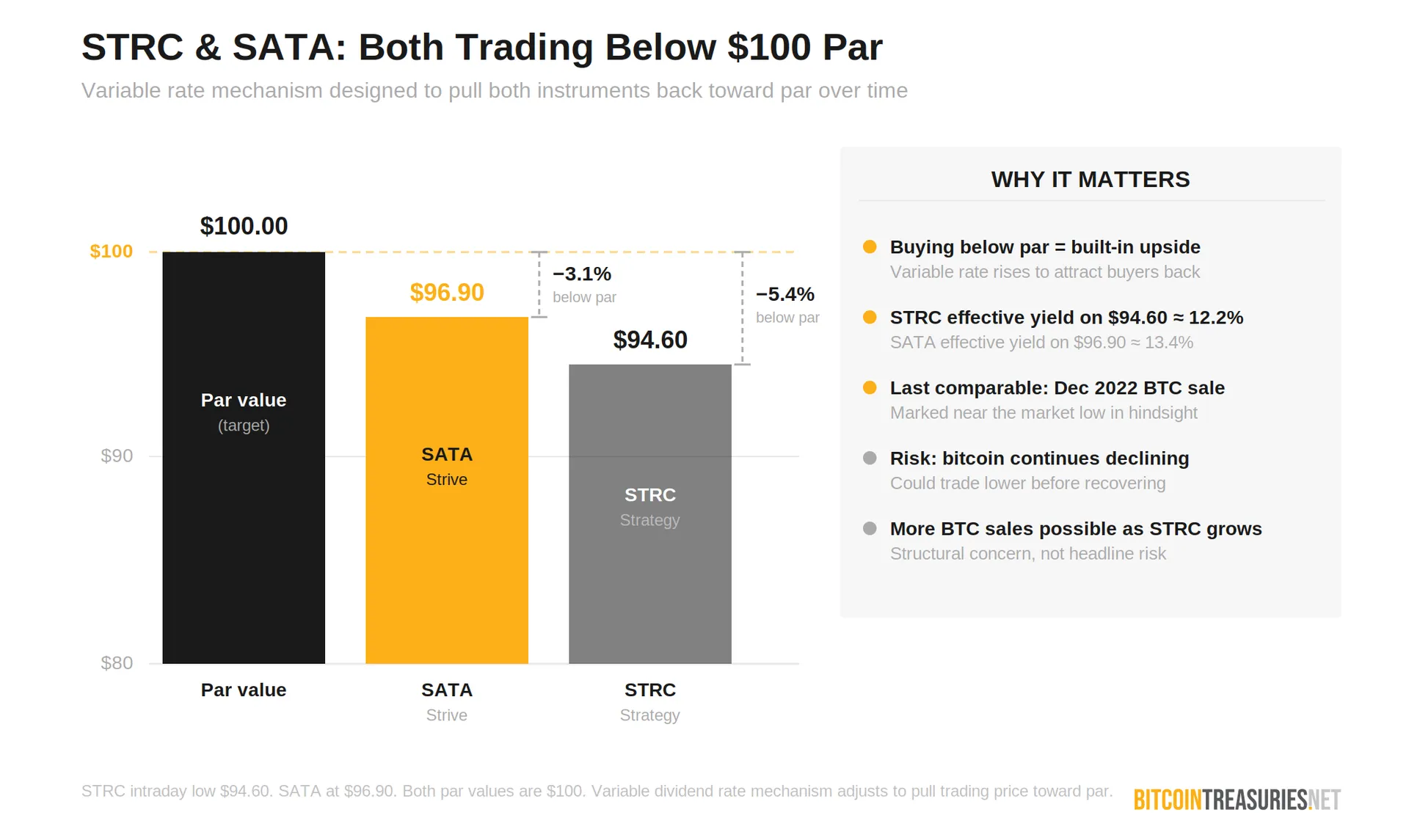

There is a number that is making a lot of people uncomfortable this week: $94. That is where Strategy's STRC preferred stock has been trading, and for an instrument engineered to stay close to $100, it is not a flattering picture. At the same time, a smaller, hungrier competitor called SATA — the preferred stock issued by Strive — is drawing real investor attention, paying a 13% annual yield, currently trading at $96.90, and about to make Wall Street history by becoming the first publicly listed security to pay dividends every single business day.

So which one do you buy? Do you buy either of them right now, with bitcoin sliding toward $65,000 and the broader crypto market rattled? And if you have been waiting for a moment where one of these instruments looked like a genuine opportunity, is this that moment?

Those are the right questions. The answers are not as simple as picking the higher yield.

A quick recap of what happened. Strategy, which holds 843,706 bitcoin as of May 31, disclosed in an 8-K filing that it sold 32 bitcoin between May 26 and May 31 at an average price of $77,135 per coin, generating approximately $2.5 million. The proceeds went directly to fund distributions on STRC. The sale was Strategy's first net bitcoin disposal in four years, and while 32 coins against a treasury of over 843,000 is roughly 0.004% of holdings, the symbolism hit hard. Michael Saylor built an identity around never selling. That identity just cracked, just a little, but enough for markets to notice.

STRC dropped to an intraday low of $94.60 on Tuesday. That is a three-month low, and it matters precisely because the entire pitch of STRC is stability. When you buy a preferred stock anchored to $100 par value, you are not supposed to be watching it trade six points below that.

By contrast, SATA is currently trading at $96.90 — closer to its $100 par value and holding up notably better than its larger rival during this week's turbulence.

The comparison to Strategy's December 2022 bitcoin sale is not unfair. That sale also happened near a market low, which in hindsight marked one of the better buying opportunities in the asset's history. Some investors are now making exactly that bet: that STRC at $94 is close to a floor, that the instrument's mechanics will pull it back toward par, and that the downside from here is limited while the upside is a return to $100 plus the 11.5% annual yield you collect along the way.

That is a legitimate thesis. It is also not the whole picture.

To understand what STRC and SATA are actually offering, you need to understand the structure these instruments are built on. Both are perpetual preferred stocks. Neither converts to common equity. Both are designed to trade near $100 through a variable dividend rate that adjusts to pull the price back to par when it strays — when the stock trades below $100, the rate goes up to attract buyers; when it trades above, the rate comes down. Monthly cash payments flow from each, classified primarily as return of capital for tax purposes, which reduces your cost basis rather than triggering ordinary income tax immediately. Both are cumulative, meaning unpaid dividends accrue. And both are backed by bitcoin balance sheets, not by operating cash flows.

That last point is the one most retail investors underweight.

Neither STRC nor SATA is collateralized by specific bitcoin holdings. You do not have a direct claim on a vault of coins. You have a claim on the issuer's balance sheet. Your protection is the issuer's ability to keep accumulating bitcoin, maintain capital markets access, and service its obligations. The difference between the two instruments is, at its core, a question of how much cushion sits beneath you.

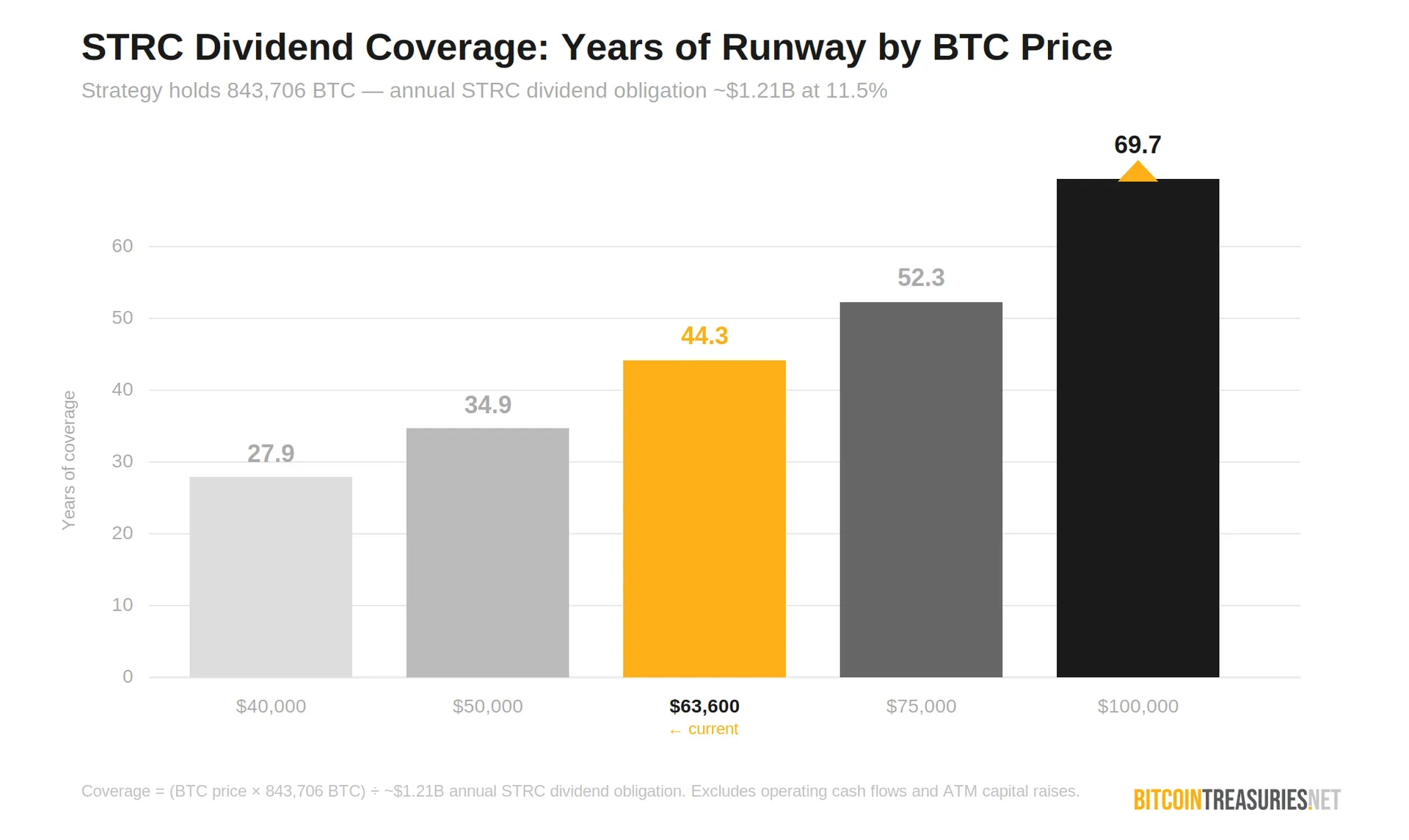

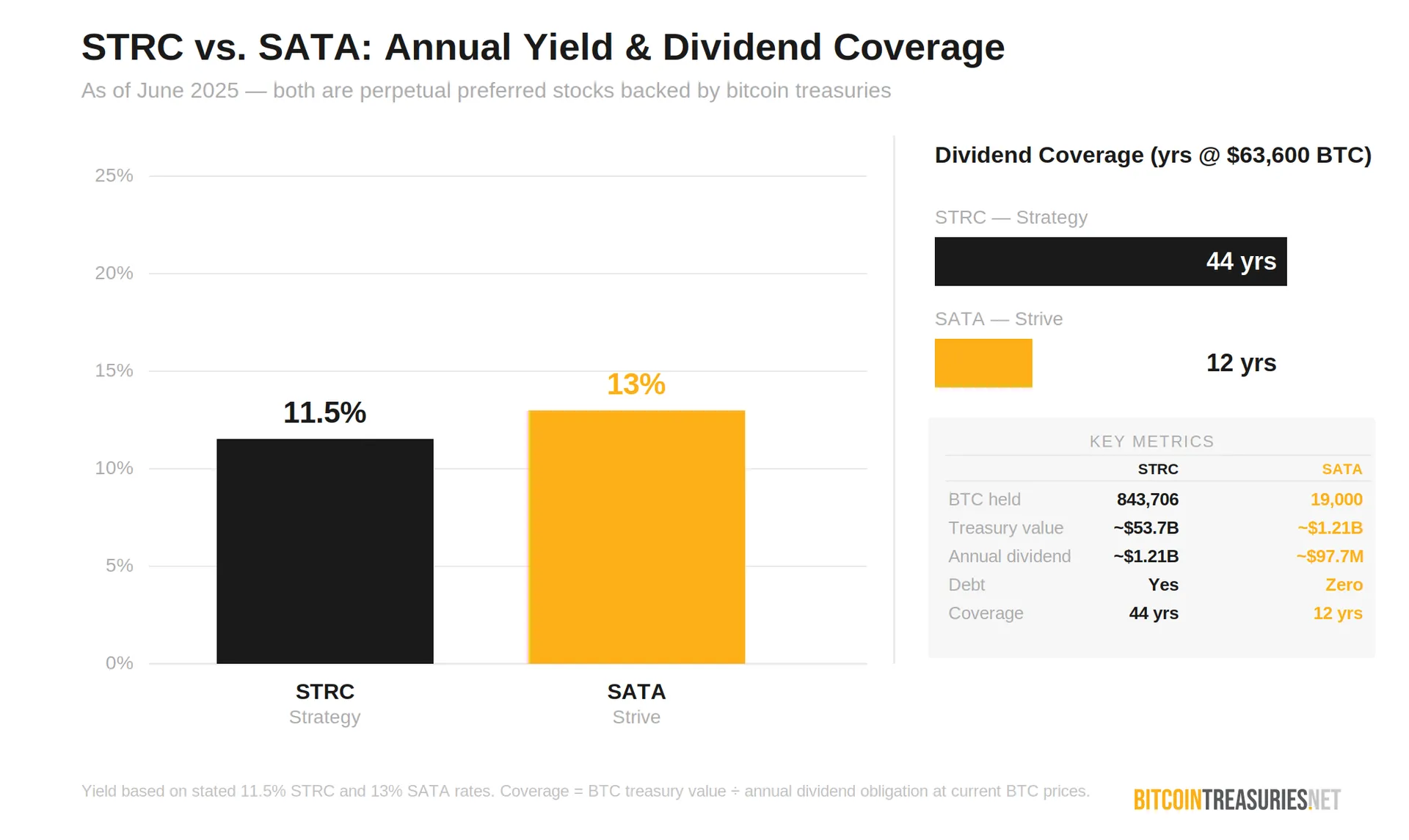

Strategy holds 843,706 bitcoin, acquired at an average cost of $75,699. At today's price of roughly $63,600, that position is worth approximately $53.7 billion. STRC has grown to $10.5 billion outstanding, and at 11.5% annualised that puts annual dividend obligations at approximately $1.21 billion per year. At current bitcoin prices, Strategy's holdings represent roughly 44 years of coverage. At $50,000 per bitcoin you are looking at around 37 years of runway, and at $40,000 — a level that would represent a brutal further decline — still around 30 years before the math gets genuinely troubled. The company also has a legacy software business generating operating cash flow, $900 million in cash reserves, and a suite of capital-raising tools including the ATM program that raised $128.3 million in the same week it sold those 32 coins.

The 11.5% yield on STRC is not an accident. It reflects this creditworthiness. You are being paid less because you are taking on less risk relative to the asset base backing you.

SATA is structured identically but built on a smaller foundation. Strive holds 19,000 bitcoin as of June 1, having added 2,500 coins in the final week of May alone at an average of $74,092 each. At today's price that treasury is worth approximately $1.21 billion. SATA now has 7.51 million shares outstanding, which at 13% puts annual dividend obligations at roughly $97.7 million per year. That gives coverage of approximately 12 years at current bitcoin prices — far less runway than Strategy, which is precisely the risk the higher yield is compensating you for. Strive has zero debt, all bitcoin unencumbered, $137.3 million in cash as of June 1, and maintains an 18-month dividend reserve in cash and liquid securities.

The 13% yield compensates you for the smaller balance sheet. Strive is not Strategy. It does not have Strategy's scale, its secondary market liquidity, or its institutional profile. A large institution cannot easily park $500 million into SATA without moving the price. STRC has that depth. SATA is building toward it.

SATA's relative price resilience — holding at $96.90 while STRC has slid to $94 — may itself be a signal worth noting. An instrument trading closer to par during a sector-wide drawdown is either better insulated from the specific concern spooking the market, or it has less institutional selling pressure, or both.

The question of whether to prefer higher yield or more scale is the core trade-off, and it is a genuine one. Some investors hold both for exactly this reason — you get STRC's institutional grade cushion alongside SATA's higher cash flow, and you diversify single-issuer risk in a space where concentration is a real concern.

What SATA brings that STRC does not is a structural innovation that deserves credit. Starting June 16, SATA becomes the first publicly listed security in U.S. capital markets history to pay dividends every single business day. That is not a marketing gimmick. For investors whose financial lives are built around regular income — retirees, income-focused funds, anyone managing monthly expenses from a portfolio — the ability to receive cash every trading day represents a genuine change in how a security functions. Strive CEO Matthew Cole called it a zero-to-one innovation, and while you can argue about the framing, he is not wrong that no listed security has done this before.

Strive also made a notable move in its Q1 report: the company holds $50.5 million in STRC preferred stock on its own balance sheet. That is Strive buying Strategy's product with real money. It is also the kind of signal that tends to get missed in headline-driven coverage but tells you something about how the two companies view each other's instruments.

Now to the harder question. Should you buy either of these right now?

The case against waiting is actually stronger than it might feel in the middle of a drawdown. These instruments are not designed for people chasing bitcoin's upside. They are designed for people who are long-term bullish on bitcoin but need predictable income — the investor who believes bitcoin belongs in a portfolio but cannot stomach watching their retirement savings drop 45% alongside it. A retiree with a 20-year time horizon does not need bitcoin volatility. They need the quiet accumulation of 11.5% or 13% cash yield against an asset that has appreciated at 30% to 50% CAGR over long arcs. The volatility in the underlying does not necessarily impair the preferred; it is the preferred structure's whole point.

The case for waiting is equally coherent. If bitcoin continues to fall and sentiment around corporate treasury companies deteriorates, STRC could go lower before it goes higher, and SATA could face widening spreads as investors reassess the sector. The bitcoin sale by Strategy spooked people not because of its size but because of what it implies: that as STRC issuance grows, bitcoin sales to fund dividends may become more frequent. That is a structural concern, not a headline risk. It deserves scrutiny.

The more precise framing is this. STRC at $94 prices in significant uncertainty. If you believe Strategy's balance sheet is not impaired — 843,706 bitcoin, $900 million cash, $128 million raised in the same week as the sale — then $94 is almost certainly below fair value for a $100 par preferred paying 11.5%. The variable rate mechanism exists specifically to pull the price back to par. That does not mean it happens immediately or linearly. But the math works in one direction when you buy below par.

SATA is a different calculation. At $96.90, it is not distressed. It is gaining momentum. The daily dividend launch on June 16 is a real differentiator, the bitcoin accumulation has been aggressive, the balance sheet is clean, and 13% against a debt-free issuer with a growing treasury is genuinely attractive. The risk is not imminent; it is structural — if bitcoin falls hard enough for long enough, a smaller treasury faces pressure faster than a larger one.

Both instruments share the same existential dependency: continued capital market access and bitcoin's long-term trajectory. Neither is FDIC insured. Neither has a direct lien on specific coins. Neither works if bitcoin goes to zero and stays there. But if you believe, as both companies' investor bases do, that bitcoin is a multi-decade store of value still in early institutional adoption, then the question of which preferred stock to own is mostly a question of how much yield premium you require to accept Strive's smaller scale relative to Strategy's institutional depth.

For the long-term income investor, the answer might simply be: both.

Want more bitcoin treasury coverage in your search results? Add Bitcoin Treasuries as a preferred source on Google.