Saylor’s STRC Moment Arrives: Institutions Now Own $2.1B in Digital Credit

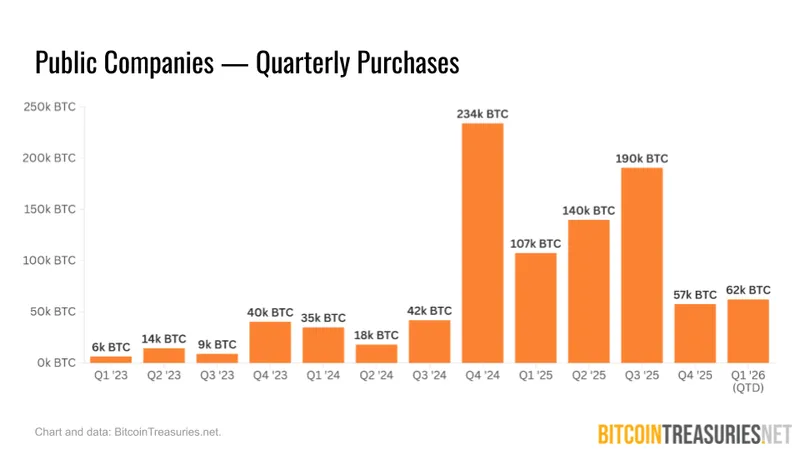

February delivered a stark reversal in corporate Bitcoin momentum: 7,800 BTC was added to treasuries but was entirely offset by sales and balance-sheet reductions.

That marks the first month of negative change since we standardized our data, yet Q1 is off to a strong start with 62,000 BTC in net additions to date, mainly from Strategy.

As Bitcoin buying fluctuates, one question dominates: what’s next for the sector? The answer is digital credit and preferred shares, now a central focus for both Strategy and Strive, allowing companies to finance Bitcoin buying while offering high yields.

This month’s edition of the BitcoinTreasuries.net Corporate Adoption Report spotlights the rapid expansion of these structures, with new data showing exceptional performance across selected preferred share classes and rising institutional participation.

As we see it, direct accumulation is variable, but the financial architecture of corporate Bitcoin ownership is only deepening.

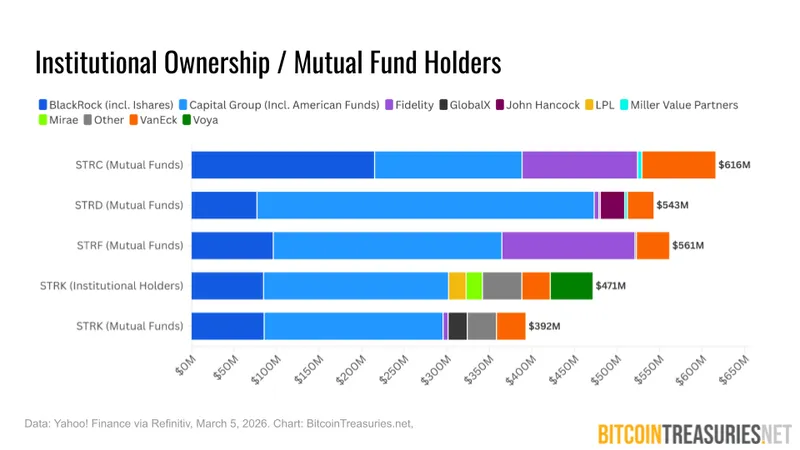

1. Institutions own $2.1 billion in digital credit

Examining Yahoo! Finance data, we find at least $2.1 billion in various digital credit instruments held by mutual funds and ETFs. That data also shows $471 million in institutional holdings of STRK, with overlap between the two categories unclear.

We see this as a critical trend, as institutional holders provide access and liquidity to retail investors while signaling credibility to others in the financial sector, providing stability through large, long-term holdings.

2. Quarterly buying is strong despite a weak February

For the first month since standardizing our data, public treasuries disposed of more Bitcoin than they added (+7,800 BTC and -8,600 BTC for a net change of -800 BTC).

February additions were largely driven by Strategy, which bought 5,075 BTC across all its weekly purchases. That makes up 65% of all February buying and preserves the company’s dominance over sector-wide cumulative Bitcoin holdings.

But the most visible growth is net change for Q1 2026 — up about 62,000 BTC as of March 9, largely driven by Strategy’s strong buying in January and early March.

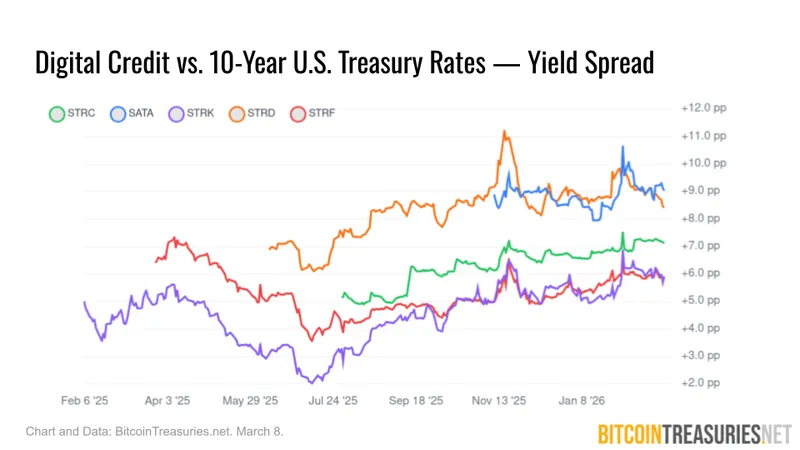

3. Digital credit offers a premium over U.S. Treasury rates

This month features findings from Bitcoin For Corporations on credit spreads — that is, how much digital credit returns compared to U.S. Treasury bonds and bills.

Their data indicates STRC’s floating-rate credit spread has a 7.60% premium over U.S. 3-month Treasury bills. Plus, three of Strategy’s fixed-rate products held steady over the last three weeks of February against 10-year U.S. Treasury bonds.

This also points to high returns. Five digital credit instruments (also including Strive’s SATA) were projected to pay out $435 million in dividends by the end of February.

Bitcoin For Corporations’ findings are supported by our own data, indicating yields above the U.S. Treasury rate for five products from Strategy and Strive.

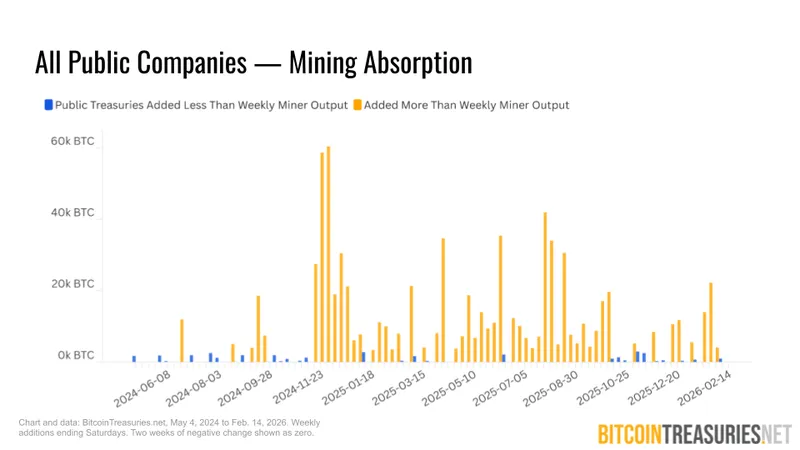

4. Treasuries are absorbing up to 2.8x mining output

Another question we delved into this month: how much of the newly mined Bitcoin supply are treasury companies acquiring?

Looking at data since the April 2024 halving, we find additions collectively outpaced Bitcoin mining output in 54 of 94 weeks that we surveyed. Over the entire period, treasury companies bought about 2.8x the amount of Bitcoin mined.

Examining Strategy alone over a shorter period, we found that it often outpaced mining output in 29 out of 67 weeks. It acquired 1.8x the BTC mined over that period.

It should be noted that BitcoinTreasuries.net includes mining companies that accumulate Bitcoin, meaning that some companies are deciding to hold much of their generated Bitcoin, and not simply buy it faster than miners can produce.

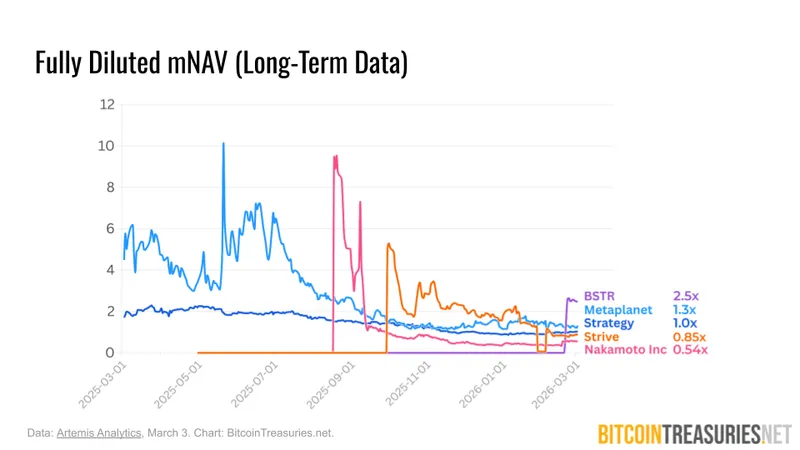

5. mNAV converges on 1.0x despite falling

Our latest findings on multiple-to-Bitcoin NAV (mNAV) point to a long-term downward trend, but also suggest that certain companies are converging toward 1.0x mNAV with a slight premium or discount.

Ryan Strauss, Managing Director at Bitcoin Consulting Group, tells us: “The market now appears to be valuing these firms more on their underlying businesses rather than simply their Bitcoin exposure ... falling mNAV ratios may not signal weakness, but rather a normalization as Bitcoin exposure becomes a more widely available and efficiently priced asset.”

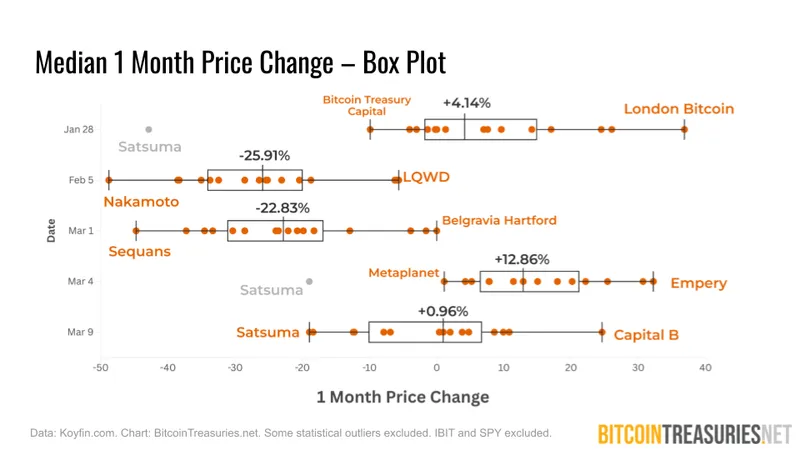

6. Market volatility evidenced by median price changes

February began with a Bitcoin price crash, but early March pointed to a moderate recovery. Treasury stocks were also volatile, largely in the red or green on key dates.

One finding: sampling certain companies we consider ”pure play” treasuries on five dates, we saw median 1-month price changes range from -25.91% to +12.86%.

Perhaps the clearest takeaway comes from comparing this to six-month price changes. Here, treasury stock price changes were firmly negative, with narrower medians ranging from -56.13% to -69.83% over five dates. This suggests that intermittent gains do not point to a full recovery from the post-summer market slide.