Inside B HODL: The UK’s First Active Bitcoin Treasury Company

The first UK‑listed company founded for Bitcoin accumulation and revenue generation from the Bitcoin in its treasury is putting its Bitcoin to work. A close look at the model Freddie New is building, and what it means for the UK's emerging Bitcoin treasury ecosystem.

In early May 2026, UK gilt yields hit levels not seen in decades - the 10-year touching 5.1%, the 30-year 5.79%. For Freddie New, CEO of B HODL Plc, this was less a surprise than a confirmation. Back in August 2025, weeks before his company listed on the Aquis Stock Exchange, New had gone public with his view that Britain was entering the early stages of a sovereign debt crisis. The market is catching up eventually. That timing mattered, not just as macroeconomic commentary, but as context for the specific kind of business New had set out to build: one engineered to be resilient, Bitcoin-accumulative, and structurally distinct from the passive treasury model that had come before it.

The Architecture

B HODL Plc listed on AQSE under the ticker HODL on September 21, 2025, raising £15.3 million in its IPO. It has since added dual listings on the OTCQB Venture Market (HODLF) and the Frankfurt Stock Exchange (F5S), expanding its public market footprint across three jurisdictions. The shareholder base signals intent: Blockstream CEO Adam Back - cited in Satoshi Nakamoto's original whitepaper - holds more than 25.5% of issued share capital. CoinCorner, the Isle of Man-based Bitcoin exchange operating since 2014, holds 14.3% and provides operational infrastructure, custody architecture, and Lightning node access under a services agreement that gives B HODL a lean operating model and a reported four-year cash runway.

The board reflects the same deliberate construction. Chairman David Jaques was the first CFO of PayPal. Allen Farrington, former investment manager at Baillie Gifford and general partner at Axiom, sits as non-executive director. Danny Scott, co-founder and CEO of CoinCorner and co-creator of the Bolt Card, serves as Chief Bitcoin Officer. The infrastructure assembled is impressive.

That strategy diverges from what came before it in a specific and articulable way. B HODL formally describes itself as a Bitcoin Treasury 2.0 company, and its mission statement compresses the model to four words: Buy. Hold. Deploy. Compound.

The distinction from Treasury 1.0 is precisely in the final two. "The old Treasury 1.0 model is the Saylor playbook of the capital stack," New told BitcoinTreasuries.Net "You sit on this appreciating asset and don't do anything with it. We want to go one step further into what we think of as a Treasury 2.0 model."

Treasury 2.0 runs on a four-step loop: raise capital, acquire Bitcoin, deploy that Bitcoin as liquidity into Lightning Network routing channels, earn routing fees, and compound those fees back into the treasury. B HODL is not a passive holding vehicle - it is a payment infrastructure business that generates Bitcoin yield.

The Lightning Flywheel

The Lightning Network is Bitcoin's Layer-2 payment rail: a system of off-chain payment channels that settle to the base layer only at open and close, enabling instant, near-zero-cost transactions at scale. Liquidity providers - node operators with capital locked into routing channels - earn fees for facilitating payment flows between counterparties. The capital itself is not consumed in routing; it cycles continuously, accumulating fees with each pass.

B HODL deploys its Bitcoin treasury as the liquidity engine for this routing function. The analogy New applies for a traditional finance audience - Lightning routing fees as equivalent to Visa or Mastercard interchange - is commercially legible: the company earns a toll for moving value across the network, denominated entirely in Bitcoin.

The critical architectural point is custody. B HODL's Lightning deployment is entirely non-custodial. The Bitcoin remains cryptographically bound to the company's own nodes. If a channel partner goes offline or acts maliciously, B HODL closes the channel unilaterally and the Bitcoin returns to cold storage. The 2022 collapses of Celsius, BlockFi, and FTX - each involving custodial third-party lending of Bitcoin - are the explicit negative template this model was designed to avoid.

Early performance exceeded internal projections. The company's initial annualised yield from Lightning routing came in at approximately 6%. Total Lightning revenue for the six months ended December 31, 2025 was £13,996 - representing only the first three months of post-IPO activity. At this stage of deployment, the revenue figure is secondary to what it demonstrates.

"Think of it as a lightning flywheel," New said. "We're earning Bitcoin every day, and your Bitcoin per share is increasing every day, but we're not diluting you."

That final clause is the operational thesis. B HODL's Lightning yield generates sats accretion without share issuance - a non-dilutive acquisition pathway delivered at the infrastructure layer rather than through the capital markets.

Capital Structure and Discipline

Equity remains the primary funding mechanism. B HODL established an At-The-Market programme on February 4, 2026, enabling incremental share sales at prevailing market prices. The programme's logic depends on the company's shares trading at a premium to the net asset value of its underlying Bitcoin. When they do - because public equity investors pay for regulated, ISA-eligible, yield-generating exposure - each new issuance buys more Bitcoin per share than it creates in dilution.

In a March 2026 issuance, the sale of 240,000 shares at 7.5p generated gross proceeds of £18,000. The resulting Bitcoin purchase achieved approximately 133 sats per newly issued share, against a then-base of roughly 116. The new shares arrived already in-the-money in Bitcoin terms. New describes this as accretive issuance: controlled dilution in share count producing anti-dilution in underlying asset concentration.

The Bitcoin-Backed Loan: Proof of Concept

Beyond equity, B HODL has introduced two debt instruments that together represent a deliberate, staged approach to financial engineering. The first is a Bitcoin-Backed Loan framework, built on CoinCorner's established lending product and approved by the full board - including independent review by chairman David Jaques and non-executive director Allen Farrington, a requirement under AQSE's related party transaction rules given CoinCorner's involvement. The parameters are tightly defined: a maximum 50% loan-to-value ratio, interest-only terms of up to four years, and an aggregate exposure cap of 20% of total treasury value.

The second is a convertible loan note - standard for institutional technology financing, but a first for UK-listed digital asset companies.

New was explicit about how these instruments are being deployed at this stage. "What kills businesses isn't balance sheet insolvency, it's cash flow insolvency," he said, drawing on his background as an insolvency lawyer. "The ability to pay your debts as they fall due is absolutely fundamental to being a going concern." For B HODL, the BBL and CLN are not leverage plays - they are proof-of-concept instruments, each tested in a controlled way before being scaled.

The BBL's first deployment came with Bitcoin trading near $70,000 - one Bitcoin purchased, the mechanism validated under live market conditions. New confirmed the company has not yet returned to the facility: "We haven't gone back to the well yet, but obviously we could." The rationale for restraint is the same rationale that governed the IPO's cash management. During the summer 2025 fundraise, New had already told prospective investors that a Bitcoin price correction was likely. The cash retained from the £15.3 million raise was deliberate. "If we held some money back in cash, we'd be able to buy Bitcoin in the future at lower prices," he said - and the drawdown from $113,000 at listing to around $70,000 by early 2026 proved the thesis.

The BBL framework exists precisely for such moments. When public share prices are suppressed and ATM issuance would be mathematically dilutive, the facility allows the company to borrow against its treasury at conservative leverage and accumulate Bitcoin at cyclical lows - without touching the core stack. The 50% LTV cap and 20% total exposure limit eliminate margin call risk across any scenario short of an extreme and sustained price collapse.

What makes the debt framework credible rather than theoretical is the self-reinforcing logic that ties it to Lightning yield. "The more Bitcoin we buy, the more we'll be able to deploy over time into more routing nodes," New said. "The more revenue we'll be able to derive, and therefore it becomes a virtuous circle - the more coming in the door, the more you can look into more leveraged instruments, because you'll be able to service that debt." The BBL and CLN are not sized against today's revenue; they are sized against where Lightning yield is going as the network grows. The conservative present-day parameters reflect that New is building the runway, not betting on it.

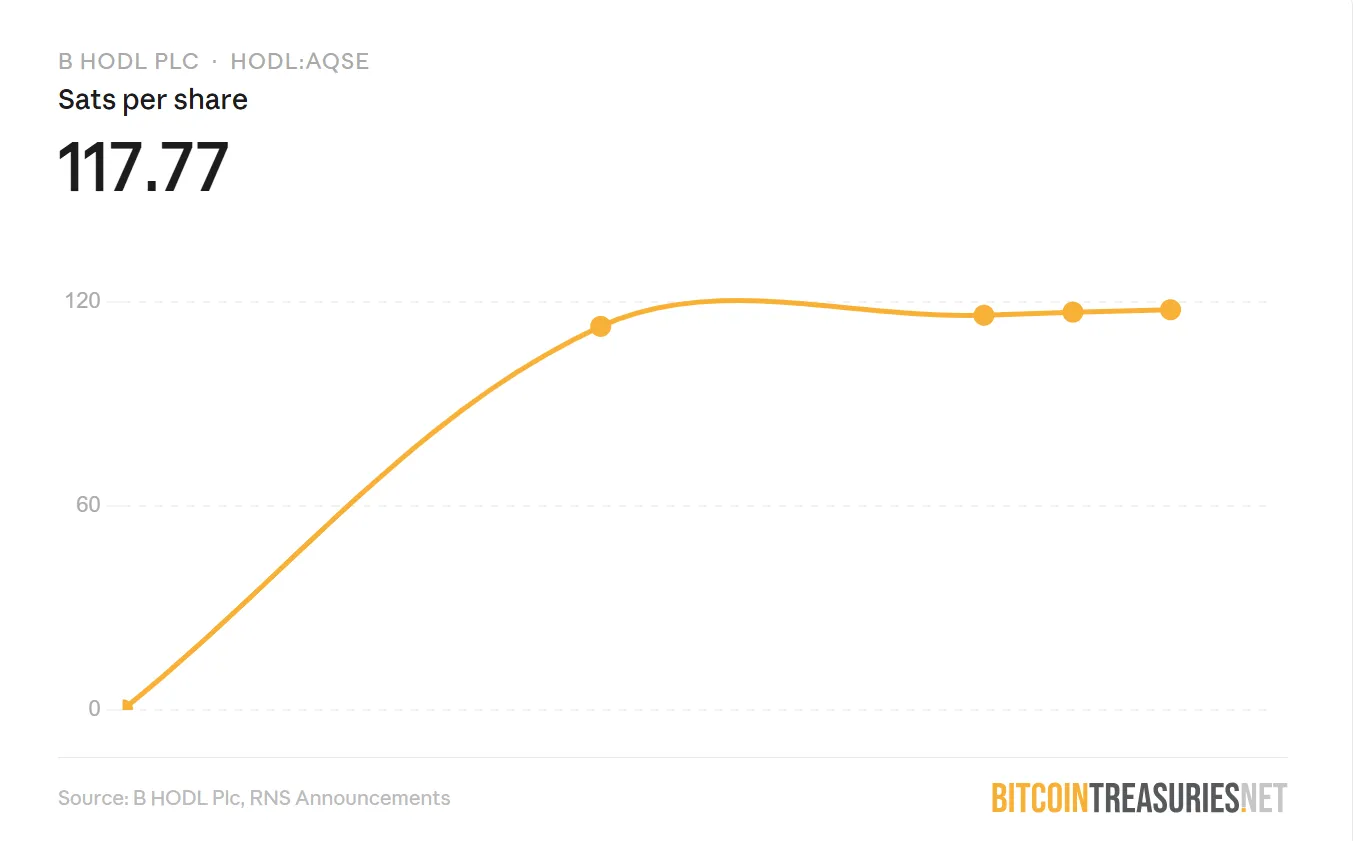

The metric B HODL publishes to track performance is sats per share - the quantity of Bitcoin, measured in satoshis, represented by each outstanding share. On December 31, 2025, the figure stood at 112.87 sats per share. By April 30, 2026, it had reached 117.77. Every ATM issuance, every Lightning routing cycle, every BBL-funded purchase has moved this number upward.

This is the correct scorecard. Fiat-denominated revenue or market cap figures describe how the stock is priced in sterling; sats per share describes how much hard money each share actually represents. The net fiat loss reported for the six months ended December 31, 2025 - £4.12 million - is largely a non-cash accounting artefact of digital asset revaluation standards. B HODL held 166.487 BTC as of April 30, 2026, and that figure compounds with every operational cycle.

Ecosystem Architecture

B HODL's relationship to the UK Bitcoin ecosystem extends beyond its own balance sheet. Upon IPO, the company committed to allocating up to 1% of capital raised and future fund returns to UK-based Bitcoin initiatives under a formal Industry Support initiative. The first grant was awarded to Brink, the non-profit dedicated to funding Bitcoin Core developer research and mentorship.

The framing New applies is commercial rather than philanthropic. "It's in our commercial interest for there to be demand for our product, which is ultimately payment services," he said. More Lightning users means more payment volume, more routing fee income, more compounding into the treasury. Supporting the protocol's development is portfolio management.

B HODL sits within a growing cluster of UK-listed Bitcoin treasury companies - Smarter Web Company, Satsuma, XCE (CEO: Scott Ellam), Stack BTC, and Falcon Edge - each required, under UK listing rules, to maintain an underlying operating business in order to avoid classification as an Alternative Investment Fund. The regulatory constraint has produced an ecosystem of structurally differentiated companies. Smarter Web is a web development business. XCE operates in recruitment. Stack acquires businesses. B HODL runs payment infrastructure. They compete for capital, and ultimately for Bitcoin, but New frames the competitive dynamic as secondary to the collaborative one.

"A delegation of five or six different listed companies turning up at Downing Street is much more powerful than just one on its own," he said. "The space for listed companies in this sector is kind of growing, and it's a bit of an exception in terms of capital market activity in the United Kingdom."

That observation carries weight. At a moment when UK capital markets are searching for growth narratives, Bitcoin treasury companies have provided genuine IPO activity on both AQSE and the LSE. B HODL's commercial model - transparent, regulated, yield-generating - is precisely the empirical evidence that policy argument requires.

The Flywheel, Forward

By treasury size, B HODL remains an early-stage company. The architecture is what the long thesis is built on - a publicly listed payment infrastructure business that converts Bitcoin liquidity into routing yield, compounds that yield into deeper deployment, and tracks the result in sats per share. The flywheel becomes more powerful as Lightning adoption scales. The infrastructure is built to carry volumes far larger than currently flow through it.

The BBL and CLN are proof-of-concept instruments now. They become scaling tools as Lightning revenues grow and the board's debt service calculus changes. The ATM programme issues accretively as long as the premium holds. The routing nodes earn daily, without dilution, in any market.

Buy. Hold. Deploy. Compound. In the meantime, the sats continue to accumulate.

Want more bitcoin treasury coverage in your search results? Add Bitcoin Treasuries as a preferred source on Google.