Liquidity Without Limits: How Strategy is Rewriting the Rules of Corporate Dividends

Payment frequency is the next frontier of fixed income innovation. Strategy just filed a proxy to claim it.

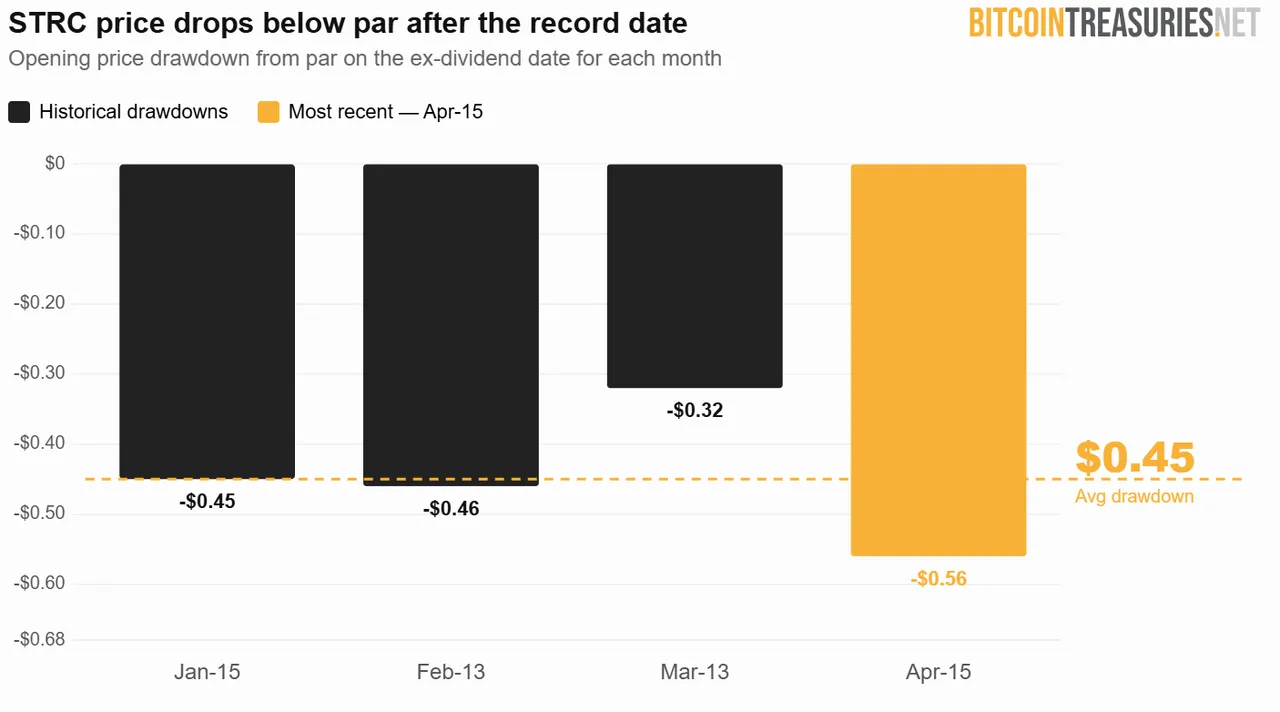

Three days after STRC's April 15 ex-dividend date, Strategy filed a proxy with the SEC. The April drop of $0.56 below par was worse than January (-$0.45), February (-$0.46), and March (-$0.32). The timing wasn’t coincidental.

The proposal is simple in structure: semi-monthly dividends on the 15th and month-end, 24 payments per year instead of 12, annual yield and total obligations unchanged at 11.5% and $1.2 billion. Strategy has been running STRC as a live engineering project for nine months, and they have now identified the one structural inefficiency that its variable rate mechanism couldn't fix, and filed a shareholder vote to address it at the exchange rule ceiling.

The problem the monthly cadence created

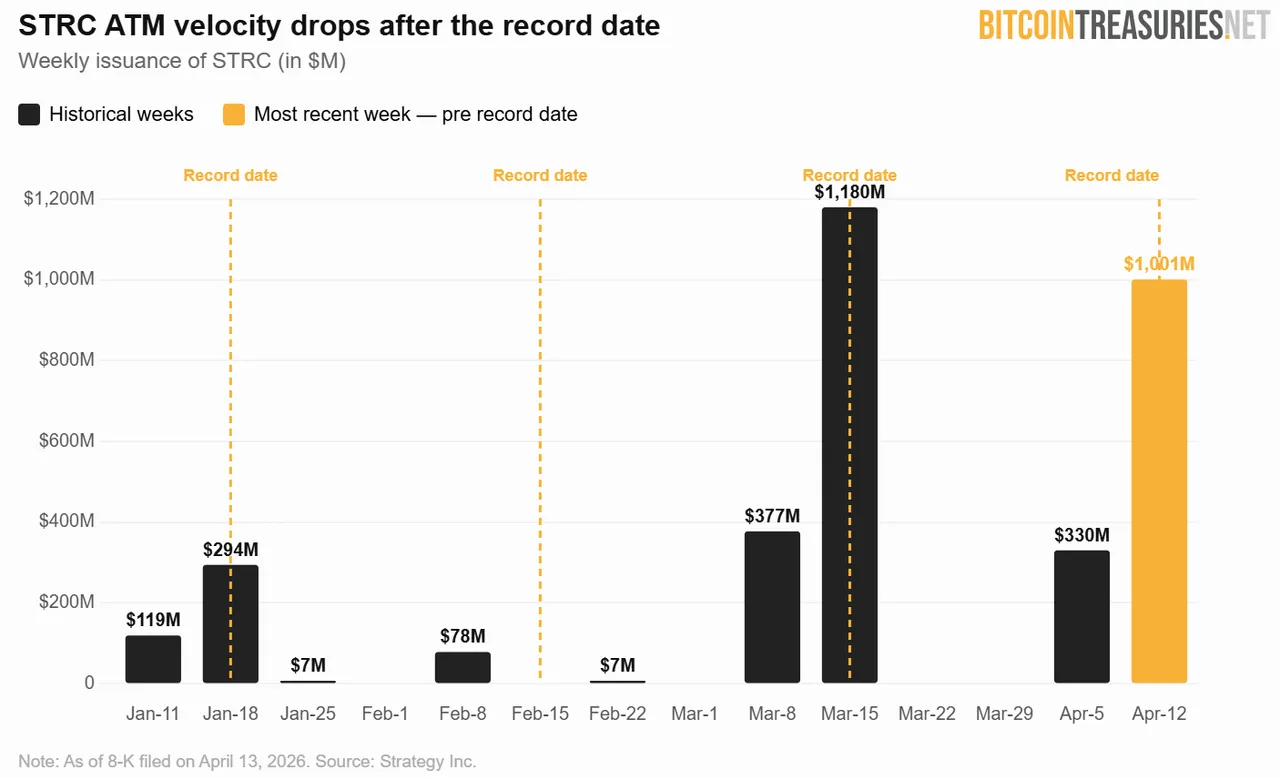

The ex-dividend pattern has been documented across eight cycles now. Not just the price drawdown, but the ATM velocity collapse that follows it. In the week ending January 25, weekly STRC issuance dropped to $7 million - down from $294 million the prior week. The swing is not a market anomaly. It is the monthly cadence operating exactly as designed, and costing Strategy the bulk of its capital-raising capacity for roughly half of every month.

That dead zone is what the variable rate mechanism cannot touch. The thermostat can adjust yield upward when STRC trades cold. It cannot manufacture demand in the two-week window after a record date when buyers who missed the cut-off have no imminent economic incentive to buy until the next cycle begins. The monthly rhythm imposes a structural tax on the instrument that is entirely independent of Bitcoin's price or Strategy's creditworthiness.

What the process reveals

In the investor presentation, CEO Phong Le disclosed that Strategy worked through dozens of iterations before arriving at semi-monthly - including weekly and daily record date structures. The Nasdaq minimum of ten calendar days between dividend declaration and record date was the hard ceiling. Semi-monthly was the most frequent structure the exchange architecture permits.

That detail reframes the proposal. This is not Strategy adding a feature to a product that is already working. It is Strategy reaching the outer boundary of what current market infrastructure allows and filing a proxy to get there. The ambition is higher frequency; the constraint is regulatory. The proposal is the intersection of both.

What the data suggests will happen

The mathematical case is direct. Each individual payment falls from $0.9583 to approximately $0.48. If the post-record-date drawdown scales proportionally to dividend size, then the opening-price drop halves from an average of $0.45 to approximately $0.22. Two smaller disruptions replace one larger one. The recovery window compresses accordingly. The dead zone doesn't disappear, but it shrinks from roughly two weeks to roughly one.

The less-discussed consequence is collateral utility. As STRC's institutional holder base - which already includes BlackRock, Fidelity, and Capital Group - increasingly looks to borrow against the position, lower and more consistent drawdowns directly improve haircuts and advance rates. A $8.5 billion instrument that holds closer to par, twice as frequently, is a materially better piece of collateral than the same instrument with monthly disruptions. The proxy explicitly identifies this as a benefit, and it compounds as the notional value grows.

Passive index eligibility follows the same structural logic. Getting into low-volatility indices is algorithmic - it requires sustained 30-day volatility below certain thresholds. At 1.7% currently, STRC is already approaching those thresholds. Cutting each individual drawdown in half tightens the band further. Index inclusion, if achieved, creates a demand channel that is entirely rule-based and independent of any individual investment decision.

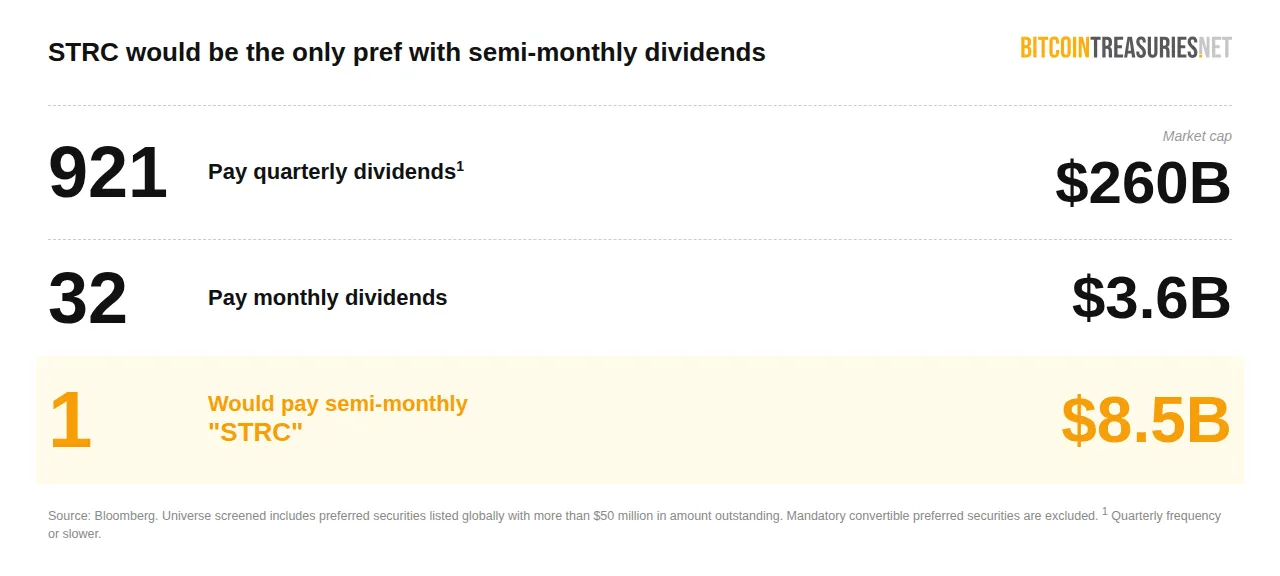

The competitive position that results is worth stating plainly. Of the globally listed preferred securities with more than $50 million in outstanding notional, 921 pay quarterly dividends representing $260 billion in combined market cap, and 32 pay monthly representing $3.6 billion. STRC at $8.5 billion would join the semi-monthly category as a product larger by notional value than the entire universe of monthly-paying preferreds.

Where is the evidence?

The standing critique of STRC - that its dividend obligations depend on perpetual capital raising - is a structural argument about the instrument's design, not a specific objection to payment frequency. It applies equally at monthly or semi-monthly cadence and is orthogonal to this proposal.

The more legitimate analytical question is whether halving the drawdown per event changes investor behaviour or simply redistributes the same friction across two smaller disruptions. No direct precedent exists to answer it. STRC would be the only semi-monthly dividend-paying instrument among more than 24,000 globally.

What does exist is directional evidence from adjacent markets. In February 2026, BlackRock filed an SEC supplement shifting both its iShares Government Money Market ETF (GMMF) and iShares Prime Money Market ETF (PMMF) from monthly to weekly dividend distributions, effective April 2026. The world's largest asset manager making that move is the clearest available signal that the premium for payment frequency is real and rising across institutional finance, not a preference unique to STRC's retail-heavy holder base.

The engineering record

STRC launched at a 9% yield, a $3 opening-price drawdown on its first ex-dividend date, and 13% 30-day volatility. Nine months later, the yield stands at 11.5%, 30-day volatility has compressed to 1.7%, and the Sharpe ratio sits at 4.53.

That compression happened because Strategy treated the instrument as a product under active development - adjusting the dividend rate monthly, managing the ATM shelf, and now proposing to restructure the payment cadence entirely.

The semi-monthly proposal is the next iteration. Strategy identified a remaining structural inefficiency that the variable rate mechanism couldn't address, worked through the available options, hit the exchange rule ceiling, and filed a proxy to reach it.

The vote is June 8. If passed, the first semi-monthly record date is June 30 and the first payment under the new cadence is July 15. The data will follow shortly after.

Want more bitcoin treasury coverage in your search results? Add Bitcoin Treasuries as a preferred source on Google.