Inside Falconedge: How One UK Treasury Firm Earns Yield in a Downturn

Falconedge was spun out of a successful 12-year-old hedge fund business with an award-winning institutional multi-strategy fund, leveraging that foundation to build a dedicated Bitcoin treasury management operation.

The product is a company that compounds sats off its own trading infrastructure rather than off its shareholders. A close look at the model being built, and where it sits in the UK Bitcoin treasury ecosystem.This includes excerpts from an exclusive interview with CEO, Roy Kashi.

This is the latest in a BitcoinTreasuries.net series deep diving into the companies developing the British Bitcoin ecosystem.

Yield Without a Tailwind

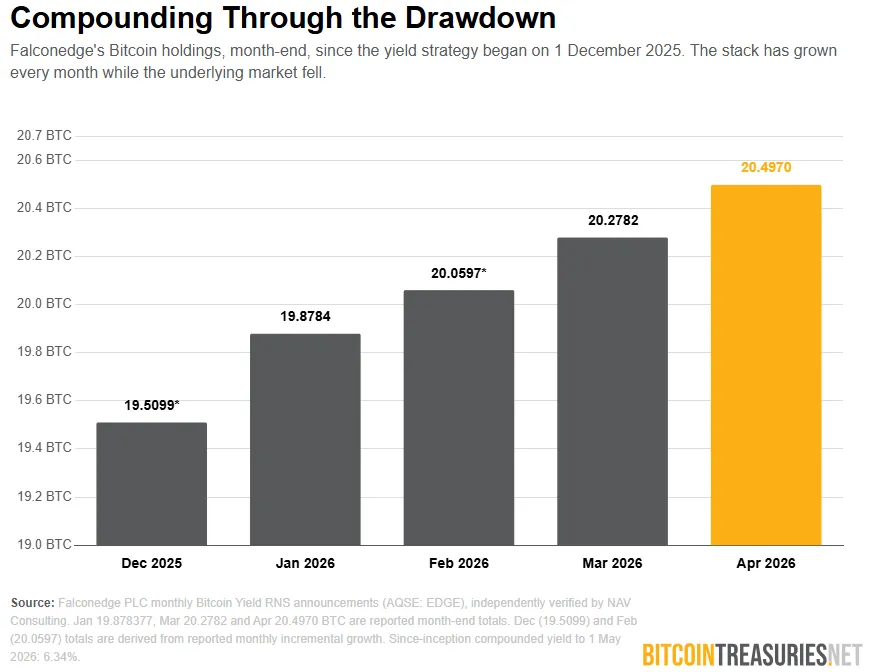

Bitcoin fell roughly 30% across the first quarter of 2026. Many treasury companies spent that quarter watching net asset value compress and waiting for the tape to turn. Falconedge spent it accumulating. For the month of April the company reported a 1.078% balance sheet yield, lifting holdings to 20.4970 BTC. Since the strategy went live on 1 December 2025, the compounded figure stands at 6.34% - 1.22 BTC of incremental growth, £70,405 in fiat-denominated return measured to 1 May 2026 - earned across a window in which the underlying asset did nothing but fall.

That is the number that defines Falconedge. The yield is, in Kashi's framing, uncorrelated to Bitcoin price action, macro events or geopolitical noise. It does not depend on a rising market, and it does not depend on issuing shares. In a sector that has spent two years debating how to acquire Bitcoin, Falconedge has built a company that grows the stack while the market falls.

The Inheritance

Falconedge listed on the Aquis Stock Exchange under the ticker EDGE on 5 November 2025, with a US OTCQB quote (FEDGF) and a Frankfurt line (V87) following. company was spun out of Falcon Investment Management, a platform ranked first in Europe by HFM in 2025 for hedge fund infrastructure and digital asset regulatory hosting. The lineage runs deep as Falcon Investment Management launched one of the UK’s first regulated crypto funds in 2018, later expanding into DeFi strategies and managing a peak of over $850 million in digital assets.

Kashi himself comes from the institutional side of the table. He was a senior portfolio manager at Brevan Howard, with further experience in oil and commodities at BGC. He likens the management profile of Falconedge to Strive in the US - a treasury company run by people with deep-rooted origins in Traditional Finance. The Bitcoin strategy, he says, came naturally as the sister company was entrenched in the asset class early, with its first fund launched around 2018. The treasury was just an extension of expertise that already existed. Kashi also spoke on the contribution of Zynx, known to the Bitcoin community as @ZynxBTC, who he spoke of warmly as a figure shaping the strategy from inside. The emphasis was on a long-term commitment to the approach that matches the company's own.

An Operating Business First

The distinction Kashi draws hardest is the one the market is slowest to hear. Falconedge is, first, an operating business with a Bitcoin strategy bolted on. The advisory arm provides turnkey infrastructure to asset and fund managers – compliance, operations, capital introduction, software, treasury strategy – the operational scaffolding that an emerging manager would otherwise need to build alone.

Falconedge departs from the wider treasury conversation with clear differentiation. The company does not watch mNAV. The premium or discount of its share price to the value of its underlying Bitcoin - the metric that governs the issuance behaviour of most of its peers - is not the variable management optimises against. The focus is the operating business and the yield it funds. Kashi is open about how he tries to block out the noise of the traditional Bitcoin treasury companies and the Saylor model with respect. Falconedge’s main objective is infrastructure that survives in both a bear and a bull market, with one stated priority above all others: maximise shareholder return.

The regulatory architecture reinforces the model. Like the rest of the UK-listed cluster, Falconedge must maintain a genuine operating business to avoid classification as an Alternative Investment Fund.

The Internal Yield Engine

The mechanism behind the 6.34% is the part of the story that sets Falconedge apart, and it is the part most treasury companies cannot replicate. The yield is generated internally and off-chain. There is no third-party lending desk, no on-chain protocol, no custodial counterparty taking the other side. The Bitcoin is put to work inside the group's own trading infrastructure - the same institutional plumbing that earned the sister platform a major European hedge fund award.

That structure removes the failure mode that destroyed the last generation of Bitcoin yield. Celsius, BlockFi and the rest were counterparty stories: Bitcoin lent out, rehypothecated, and gone when the counterparty failed. Falconedge's yield carries no such exposure. The trading managers own their own capital loss - a first-loss structure in which the downside sits with the manager, not the company. For Falconedge, that arrangement is what underwrites both the return and the preservation of capital. When asked about why someone should try to earn returns on Bitcoin, the response was “Why would you put money into a 0% savings account? You wouldn't,” Kashi says. “So you have to let it work, let it return.”

The cadence is the engine. The strategy compounds at roughly 1.2% per month - December 1.29%, January 1.88%, April 1.078% - and the compounding is the entire thesis. In a bear market the company earns Bitcoin without diluting shareholders. It accumulates through the drawdown, then carries a larger stack into the next bull market, where the same percentage yield compounds off a far larger base. The bear market builds the position the bull market amplifies. Each month's yield is reported as independently verified.

Yield to Shareholders, Not From Them

Kashi is direct about what he will not do. Heavy dilution of shareholders - the engine of the best-known treasury playbooks - makes him deeply uncomfortable. “I don't want to use shareholders as yield,” he says. “I want to provide yield to them.” The inversion is the whole point. In a model funded by continuous share issuance, the shareholder is the source of the Bitcoin the company buys. In Falconedge's model, the operating business and the internal yield are the source, and the shareholder is the recipient.

This is why the company can accumulate without an at-the-market programme running hot. The monthly yield adds Bitcoin to the balance sheet with no shares created against it; the advisory revenue adds more. Both pathways raise Bitcoin per share rather than diluting it. The flexibility to raise equity when a genuinely strategic opportunity appears remains, but it is an option, not the engine. The engine runs whether the company issues a single new share.

What Is Being Built Next

Two instruments sit on the horizon, and both were described in interview as in discussion rather than filed. They are worth setting out precisely because they show where the capital structure is heading.

The first is a fixed-coupon bond, one or two years in tenor, with a Bitcoin kicker attached. The structure is built to be asymmetric in the holder's favour: in a bear market the bondholder is unaffected and still collects the coupon; if Bitcoin rises sharply over the term, the holder participates in the upside through the kicker. It is a debt instrument designed to pay in a flat or falling market and to convert into Bitcoin exposure in a rising one - financing that does not punish the shareholder to service it.

The second is preferred equity, and Kashi's framing of it is structural. He points to a comparison made by Matt Cole at the Bitcoin Treasuries Conference – that the mutual fund and ETF industries support thirty to forty instruments – and argues the same multiplicity is coming to Bitcoin preferreds. He sees tens of different preferred instruments issued by different companies, and multiple instruments coexisting within a single region. On this reading the UK does not need one winner in preferred equity; it needs a market.

The existing capital structure is notably clean. There is no IPO warrant overhang - no warrants were issued at listing. The only warrants outstanding are held by management, who have increased their shareholdings and committed to the company. It is a structure with no hidden supply waiting to print against existing holders, which is precisely the condition under which new instruments can be added without diluting the people already on the register.

The Cluster, and the Horizon

Falconedge does not frame the rest of the UK-listed field as rivals. Kashi praises the other British Bitcoin companies as genuine businesses and stays in close contact with their teams – a collaboration that has become characteristic of the cohort. The Smarter Web Company, B HODL, XCE, Satsuma, Stack and Falconedge are each required by the listing rules to run a real operating business, and the result is an ecosystem of structurally different companies pulling in the same direction. They compete for capital and ultimately for Bitcoin, but the collective case for the sector is stronger than any single name making it alone.

On the macro, Kashi is similarly measured. Asked what one UK government policy he would change overnight, the answer is the removal of capital gains tax on Bitcoin - with the caveat that he would only expect it once the government itself adopts a Bitcoin treasury strategy. This has been a recurring theme in my discussions with the CEO’s of British Bitcoin companies.

The horizon he describes is a five-year one: Bitcoin at $1 million a coin, with Falconedge holding thousands of BTC. Stated baldly that is a conviction, not a forecast, and Kashi presents it as such. What makes it more than a number is the mechanism underneath it. A company that compounds Bitcoin off its own revenue and its own trading infrastructure, without leaning on its shareholders to do it, accumulates in every kind of market. The bear market earns the coins. The bull market multiplies them. In the meantime, the stack compounds regardless.

Want more bitcoin treasury coverage in your search results? Add Bitcoin Treasuries as a preferred source on Google.